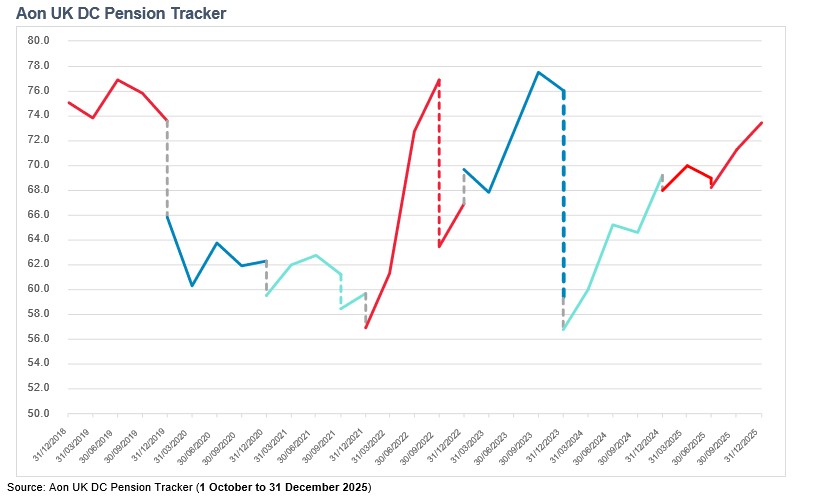

Over the quarter (October to December 2025), the Aon UK DC Pension Tracker rose, which suggests the expected future living standard in retirement provided by defined contribution (DC) savings was higher than at the end of the previous quarter.

Note, the sample savers used in the Aon DC Tracker were ‘re-set’ to their original age and fund values at the year-end which results in the discontinuity (shown in grey in the chart above) as at 31 December 2024.

The Tracker rose from 71.3 to 73.4 over the last quarter of 2025, driven predominantly by positive benchmark investment returns across major asset classes.

This has resulted in an increase in expected retirement income for all savers, though younger savers benefited the most (in percentage terms) as they also benefit from higher future return assumptions post-retirement, unlike older members who are closer to retirement.

Pensions rise in a volatile year

2025 was another volatile year with global headlines dominated by tariff announcements and persistent geopolitical tensions that unsettled markets and created a challenging environment for investors. Despite this turbulence, DC pension savers typically fared well and were expected to have a higher income in retirement than they were at the start of 2025.

Expected retirement outcomes were also supported by a relatively small increase in the Retirement Living Standards during the year which was more than offset, at the minimum and moderate target levels, by the April increase in the State Pension.

While 2025 finished on a high for pension savers, the start of 2026 has brought further market volatility from geopolitical events. Continued uncertainty around ongoing energy supplies means the spectre of inflation is looming large over the global economy once again. This prospect of higher inflation has the potential to erode the real value of retirement incomes for pension savers and put pressure on household budgets. This may lead to a reduction in the amount people can afford to save for the future. It will be interesting to see how our sample savers fare during 2026.

New Living Standards on the horizon – more Snakes and Ladders for DC Savers?

Despite the volatility, benchmark investment returns have typically been remarkably good in the last few years for DC pension savers, who have climbed metaphorical ladders towards higher retirement incomes. Many individuals will have seen their pension funds grow ever higher over the period. However, with Pensions UK expected to release revised Retirement Living Standards during 2026, savers may be about to land on a ‘snake’ which would return their retirement expectations to where they were previously.

If earlier Tracker updates are anything to go by, and as seen in 2022 and 2023, climbing the ladder of positive returns can quickly be undone when an increase to the Retirement Living Standards effectively raises the bar for savers. Members may feel themselves sliding back down towards a lower standard of living as a result.

Matthew Arends, partner and head of UK Retirement Policy at Aon, said: “While everyone’s expectations of an ‘adequate’ retirement income will differ, any change to the Retirement Living Standards, particularly an increase, will require DC savers to reassess their positions and consider whether additional savings, or working longer, may be required to achieve the living standard they want in retirement.

“The recent jump in oil and gas prices is driving another surge in inflation which will add more pressure to household budgets. Understandably, people may find it difficult to maintain or even increase pensions savings against this backdrop. When coupled with the expected increase in the Retirement Living Standards, many savers may see a comfortable retirement slipping further out of view.”

Movement over the last quarter of 2025

The increase in the Aon UK DC Pension Tracker over the final quarter of 2025 was primarily driven by positive benchmark performance over the period. On an individual saver basis, movements over the quarter were positive at all ages.

The youngest saver saw an increase of around £1,000 p.a. (2.7 percent) driven by positive actual investment performance over the quarter and an increase in expected future investment return assumptions both pre- and post-retirement.

The 40-year-old saver saw the largest increase of around £1,050 p.a. (or 2.6 percent) in their expected retirement income. Again, this was driven by positive actual investment performance over the quarter and a rise in post-retirement expected future returns. These were offset to a degree by a reduction in the expected future return pre-retirement.

Our 50-year-old saver saw an increase of around £500 p.a. (or 1.3 percent) in their expected retirement income. Due to this saver’s larger existing funds, strong investment performance gave the most benefit, particularly in equity markets, over the quarter. However, this was partially offset by decreases in expected future return assumptions pre- and post-retirement.

The oldest saver’s income was broadly flat (an increase of around £50 p.a. or 2.6 percent). This was as a result of positive investment return over the quarter being almost entirely offset by a reduction in expected future returns pre- and post-retirement.

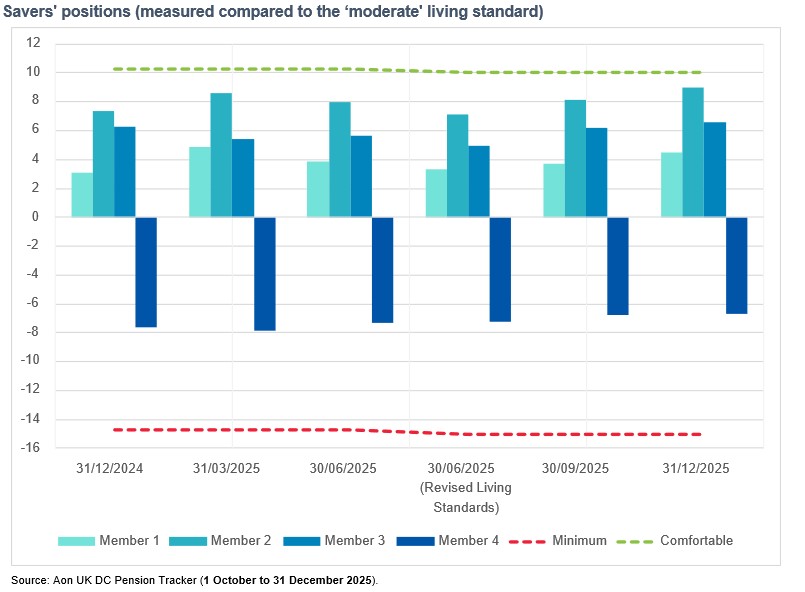

Overall, the oldest saver is expected to be the worst-off in retirement, albeit with a retirement income of around 150 percent of the ‘minimum’ Retirement Living Standard. This excludes any defined benefit pension benefits they may have but which are not included in this projection.

|