The quarterly Defined Benefit (DB) Redress Tracker from leading independent financial services consultancy Broadstone provides an indicator of the level of compensation due to those who were previously ill-advised to transfer out of their DB pension.

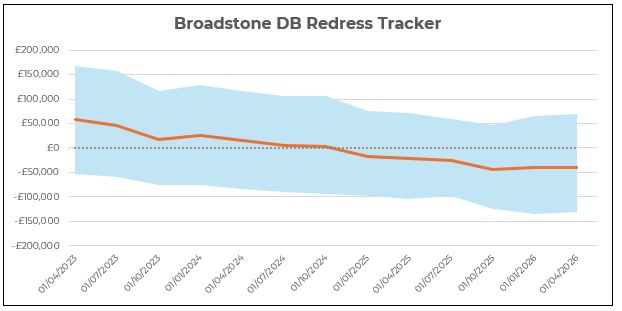

Broadstone’s DB Redress Tracker follows the example of an individual who left their scheme in 2018 aged 50, with a pension of £10,000 p.a. which would receive inflation-linked increases when in payment. The potential spread around the example case – the area shaded blue in the below chart – has been updated to reflect the largest loss and gain in a notional portfolio of cases (previously it showed a narrower spread based on varying the fund return for the single example case).

The Tracker is developed in line with Financial Conduct Authority (FCA) rules for calculating redress with the individual assumed to have invested their funds to earn returns in line with the FTSE Private Investor Index.

The most recent update for Q2 2026 shows that no redress is payable as the consumer is likely to be judged to be better off as a result of the transfer with the central estimate remaining broadly unchanged at compensation of -£40,000.

The last time that the Tracker found compensation would be payable was Q4 2024 (£2,000) with the central estimate showing a clear and sustained downward trend; three years ago, the central estimate found that £57,000 (Q2 2023) would be payable.

However, that central result hides that that there are still some consumers to whom redress will be payable as the redress evaluation will need to consider factors including:

the critical yield at time of transfer – the higher the critical yield the more likely redress is payablethe date of transfer – transfers during the period 2016-2018 will generally show a gain, whereas more recent transfers and, particularly, much older transfers are more likely to show a lossinvestment returns since transfer – consumers who have achieved relatively low investment returns post transfer, whether due to choosing low risk investments such as cash or making poor investment choices will be more likely to show redress payable

While attention is likely to focus on the impact of current global instability on redress figures, to-date there has been minimal impact scrutinising the data through March 2026.

Assets have deteriorated following the conflict in Iran and inflation expectations have spiked, but this has largely been offset by increases in bond yields.

Simon Robinson, Senior Consultant & Actuary in Broadstone’s Insurance Advisory & Remediation division, commented: “While markets have experienced a period of heightened volatility over the past month or so, the impact on DB transfer redress calculations has so far been limited. Poorer asset performance would normally increase the likelihood of redress being payable, but this has largely been offset by rising short- to medium-term bond yields, which reduce the value of the benefits that would have been given up.

“Our central estimate continues to suggest that, in many cases, redress will not be payable for most consumers. However, the headline figure does not tell the whole story and outcomes remain highly dependent on individual circumstances such as investment performance, the critical yield at the point of transfer and the timing of the transfer itself. This means that while the overall trend in redress calculations has moved down significantly over the past few years, there will still be a cohort of consumers for whom redress is payable, and firms must continue to assess cases carefully rather than assuming no compensation will be due.”

|