With the State Pension age due to start increasing from 66 to 67 in April, new research from the Standard Life Centre for the Future of Retirement highlights the difficult reality facing many over 60s who are forced to go without the basics and raid their savings in the years before they can claim their State Pension.

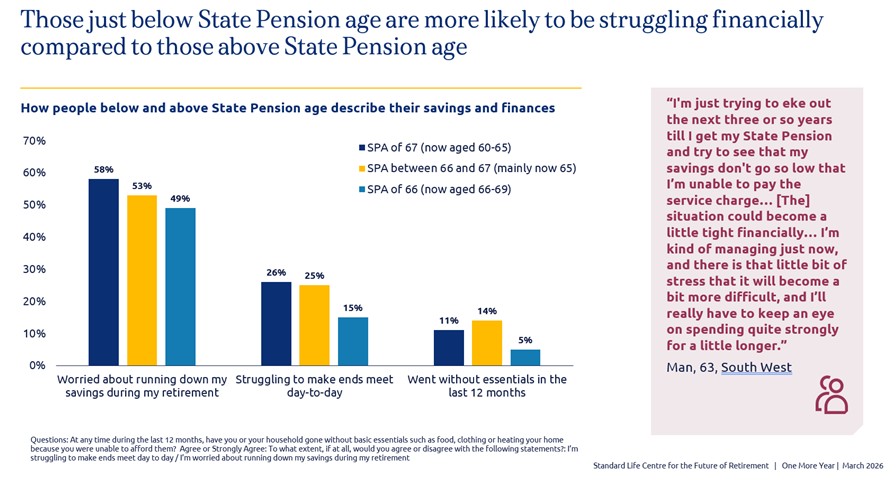

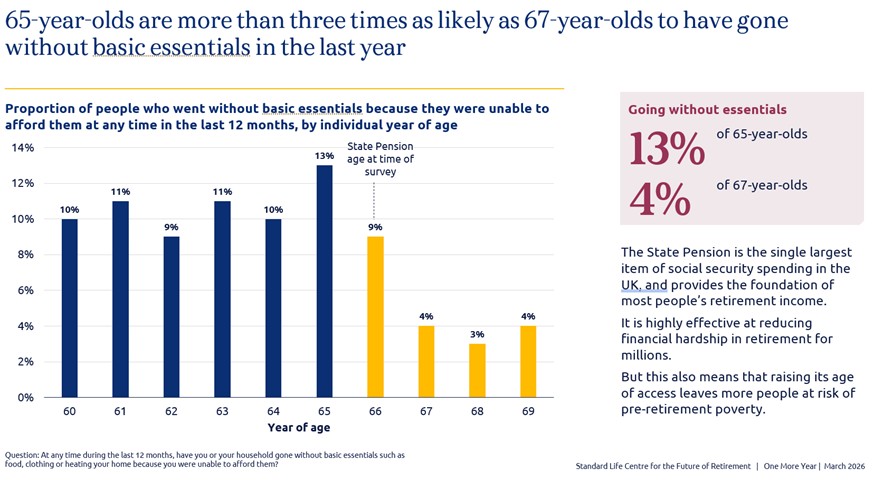

The research focused on the transition group who will be affected first by the forthcoming rise in the State Pension age and found that the group who are currently just below State Pension age are nearly three times as likely (14%) to have gone without essentials such as food, clothing or heating in the last 12 months compared to those aged 66 to 69 (5%), who are above State Pension age.

A quarter (26%) of people in their early 60s said they currently struggled to make ends meet on a day-to-day basis, compared to one in seven (15%) people above State Pension age.

The research chimed with recent analysis from the Standard Life Centre for the Future of Retirement, which showed that 250,000 more 60–64-year-olds were living in relative income poverty compared with in 2010, largely because of increases in the State Pension age.

Rising State Pension age impacts financial security

A fifth (21%) of people earning less than £25,000 said the rise in the State Pension age will have a major impact on their household finances, compared with just 10% of those earning £50,000 or more, highlighting that the impact of the changes is not evenly spread.

The significance of the State Pension to low-income households is stark. For the poorest fifth of households that include someone aged 66–70 and where no one is in paid work, the state pension makes up nearly three quarters (71%) of their income3. There is also a looming generational challenge, with a majority of Gen X – the oldest of whom are now in their 60s – projected to be highly or entirely dependent on the State Pension4.

Many say they will work for longer to offset the challenges presented by State Pension age rises

The research found that, for many, continuing in work is needed to help bridge the gap until they reach their State Pension age. Among non-retired people in their early 60s, who will be affected by the upcoming State Pension age rise, more than a third (36%) say they will need to work for longer because of the rise. One in twenty (5%) of those who are impacted by the rise, but currently say they have retired, say they plan to go back to work, as the financial reality of retirement falls short of expectations.

A quarter (23%) of those in their early 60s say they will draw down on savings or a pension, and 8% say they will apply for Universal Credit or other benefits to ‘bridge the gap’ to a higher State Pension age, showing that many costs will be diverted elsewhere.

People aged 60 to 65 are also more likely than those above State Pension age to say they are working because they need money for day-to-day expenses (38% vs 31%), to save more into their pension (31% vs 25%), and because they are worried they don’t have enough saved in their pension for retirement (25% vs 18%).

Patrick Thomson, Head of Research Analysis and Policy at the Standard Life Centre for the Future of Retirement, comments: “The rise in State Pension age is less than a week away and, while most people impacted know it is coming, they really don’t like it. Many say the change makes them feel pressured, anxious or insecure.?

“Most people affected expect the increase to impact their finances, retirement choices or health - and are making changes to adapt - working longer, saving more, or drawing down on savings.?

“While some are able to adapt to these changes, others will face real financial hardship. 14% of those just below State Pension age have gone without basic essentials in the past year. Women are significantly more impacted than men, as are those on lower incomes, who rely more on the State Pension.

“We face a growing crisis in which too many people in their 60s are struggling to make ends meet as the State Pension age rises. Without action, this will worsen the widespread pension under-saving problem, and government must set out a clear plan to improve financial security so the most vulnerable are supported before and during retirement.

“While some say they will work for longer, around one in four are expecting to draw down on their own pensions or savings to bridge the gap. That will leave people less financially secure in retirement. “The move from 66 to 67 is expected to save the government about £10 billion a year, but this data shows that some of that will be diverted from people’s own retirement savings, or from people applying for other benefits.

“We need to focus on helping working carers, those with health conditions, and to support people with lifelong learning and to make career moves that work for them. This will help people bridge the gap to State Pension age, and help retain the valuable skills and experience needed in the economy.

? “We need to help those still unaware of the upcoming changes, and support those most at risk of financial hardship resulting from the rise. We also need to plan ahead for any future changes to the State Pension age, particularly with the government currently reviewing the plan for the further rise to 68.”

|