Mortgage advisers are in a privileged position to add value and provide a more holistic view of clients’ finances by discussing the importance of protection following the purchase of a home.

The majority (76%) of homeowners discussed protection products during their initial session with their broker, with life insurance being the most commonly purchased product (57%), followed by critical illness (36%) and income protection (31%).

However, more than one in ten (13%) did not discuss protection at all, rising to a fifth (20%) of those aged 55 and above – despite this age group being more likely to suffer from health concerns.

Homeowners question if they can afford or need cover

More than one in four homebuyers who did discuss protection did not go on to make a purchase (28%), leaving them unprotected as a result.

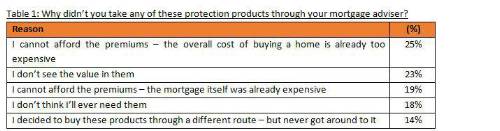

Of these, 25% rejected the opportunity to take out cover because they felt they couldn’t afford the premiums, as the overall cost of buying a home was already expensive. A slightly smaller proportion (19%) felt they could not afford the cost as the mortgage itself was costly.

Nearly a quarter (23%) didn’t see the value in protection products, while 18% thought they would never need them. One in seven (14%) intended to purchase protection through a different route, but never got round to it. Could mortgage advisers close more of those sales with the right tools and support from protection providers?

Alarmingly, two in five homeowners (42%) could only cover essential bills for up to two months if their household lost its primary income, and a further 30% could only extend to six months. Adequate financial protection is therefore vital to ensure households can keep up their mortgage payments and retain possession of their home should they unexpectedly lose their income.

Among those who discussed protection but did not make a purchase, leaving them unprotected. Homeowners who didn’t make a purchase because they already had protection in place have been removed from the base.

Natalie Summerson, Head of Sales for Individual Protection at Canada Life comments: “Buying a house is the biggest financial obligation many of us will take on in our lifetime. It’s an obvious moment to pause and consider your protection needs.

“Nobody wants to run into financial difficulty, but homeowners should have a plan to continue paying their mortgage if something happens to their main source of income. Relying on savings isn’t viable for many, and certainly isn’t good for financial resilience.

“Advisers have an open door to make sure their clients understand the importance of putting appropriate protection in place. By taking a rounded view of their client’s finances, circumstances and needs, brokers can prove their value beyond just mortgage advice.”

|