Despite considerable economic and political uncertainty during 2016, the average pension fund finished the year up by 15.7%. This is the fifth consecutive year of positive pension fund growth and will be welcome news not only to those saving into a defined contribution pension scheme, but also the growing number of retirees who remain invested in pension funds by opting for income drawdown.

Of all the pension funds surveyed, the vast majority (94%) delivered positive growth during 2016. In terms of the leading ABI pension fund sectors, Commodity/Energy (70.9%), Global Emerging Markets (32.4%) and North America Equities (31.2%) led the way.

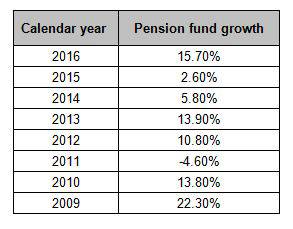

Table 1: Average annual pension fund returns (Source: Moneyfacts Personal Pension and Annuity Trends Report/Lipper)

Richard Eagling, Head of Pensions and Investments at Moneyfacts, said: “Defined contribution pension schemes and income drawdown are in the spotlight like never before. The record numbers saving into defined contribution pension schemes and using income drawdown have placed even greater importance on the ability of funds to deliver strong performance if individuals are to have any chance of generating a reasonable retirement income.

“For all the economic and political uncertainty that 2016 brought, it will be remembered as a productive year for the performance of most pension and drawdown funds.”

The Moneyfacts Personal Pension and Annuity Trends Treasury Report, out later this month, provides a comprehensive review of the UK personal pension and annuity sectors, with detailed analysis of annuity rates, pension fund returns and maturity values.

|