|

|

Although State Pension income is the biggest source of income for around half of retired households, almost four in ten people fail to check their State Pension forecast before stepping back from work, new research from Just Group shows. Among those who did check, 14% said their forecast was less than they had expected with about half of them saying that it was £500 per year less than they had anticipated. |

Stephen Lowe, group communications director at retirement specialist Just Group, said that the State Pension as a source of income is too important to leave to chance.

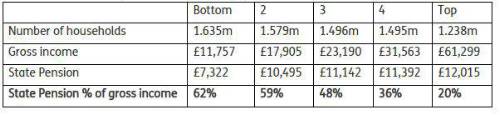

State Pension as a % of gross annual income by quintile for retired households “State Pension makes up about half or more of income for 4.7 million of the 7.5 million pensioner households, so it is crucial people track how much they are likely to receive,” he said. “It’s good that about six in 10 did check what they will get but that still leaves significant numbers, including a slightly higher proportion of women (39%) than men (35%), lacking this important information. “Significant numbers of people – again about four in 10 – retired with no financial planning while one in 10 men (10%) and almost one in five women (17%) said they had no time to plan.” He said that of the 24% who said their forecast was not what they were expecting, a third said it was between £250 and £500 less, a quarter it was more than £500 less, a third it was £250-£500 more, and about one in 10 it was £500 more. Once receiving their State Pension, 85% said it was what their forecast had led them to expect. “Ideally, people should know exactly what their income is going to be before making the decision to retire because that’s the only way to ensure giving up work is affordable,” said Stephen Lowe. “In the real-world retirement can arrive unexpectedly, perhaps due to poor health or redundancy.

“Those shocks are easier to deal with if people have started considering their options from their early 50s, for example, by getting a State Pension forecast, taking professional advice or the free, independent and impartial guidance available from Pension Wise, the government’s service.” |

|

|

|

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd