Recent financial market volatility driven by the prospect of global trade wars has highlighted how unpredictable markets can be when uncertainty abounds, and for over 50’s, the consequences are particularly significant. New research from Standard Life, part of Phoenix Group, examines how this group thinks about market uncertainty in relation to their retirement and finds that two fifths (41%) of those yet to retire expect their risk tolerance to reduce as they approach retirement

Three-quarters (76%) of over 50’s cite appetite for risk as an important factor when deciding what to do with their pension pot, according to the findings. This suggests that the vast majority of people are aware that they either have less time to recoup losses ahead of retirement or may be running down their savings more quickly if taking an income from a pension in drawdown. Just 8% of over 50’s yet to retire anticipate an increase in their appetite to take on more risk with their pension savings as they approach retirement, potentially driven by a desire to close a savings shortfall.

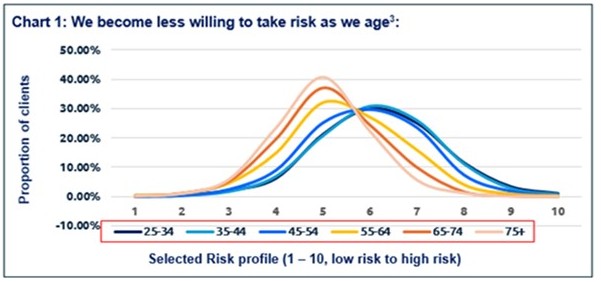

These broad trends mirror data from Dynamic Planner which demonstrates how we become less willing to take risk as we age, with tolerance to risk steeply tapering off at the point we head into retirement.

The ‘Retirement Risk Zone’

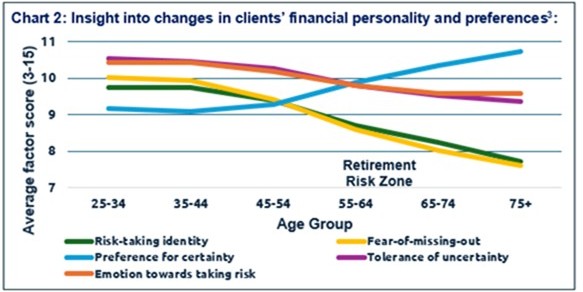

Retirement savings are particularly vulnerable to market ups and downs during the ‘Retirement Risk Zone’ – the critical period five to ten years before and after retirement. During this time, many may want to remain invested to continue growing their pension savings, but at the same time worry about market volatility given how close they are to retirement. Indeed, Dynamic Planner’s Financial Personalities research highlights that the Retirement Risk Zone is the critical period during which the preference for certainty significantly overtakes a preference for risk-taking, as well as the fear of missing out on potential investment growth.

An individual’s financial personality can often change as they approach retirement. The stakes of investing are significantly higher than earlier in the accumulation journey, and preferences can shift from taking financial risks to preferring greater certainty of future investment values and retirement outcomes. As Chart 1 shows, there is a significant reduction in appetite for risk as we age, while Chart 2 highlights that attitudes towards investment risk also steadily reduce with age, alongside the fear of missing out and tolerance of uncertainty, in favour of a significant preference for certainty.

Claire Altman, Managing Director of Individual Retirement at Standard Life, commented: “Investment risk is an ongoing area of focus for regulators, the industry and customers. The FCA’s Retirement Income Review highlighted that decisions for those approaching or in retirement have become much more complex with the potential for more risk, with a focus on the level of income withdrawn and the investments where savings are held. Attitudes towards risk will differ from person to person, but recent market volatility has clearly shown the impact this can have on an individual’s pension savings. Research from Oxford Risk has also shown that emotional reactions to market movements costs the average investor around 3% per year in lost returns.

"This is especially true for those in the Retirement Risk Zone, when many may be thinking about or already withdrawing their pension savings. During this time retirement savings are more vulnerable to any major losses which could have a knock-on impact on someone’s retirement lifestyle. Retirement income products, such as smoothed managed funds, offer a solution to the conundrum around investment growth versus risk, and over half (56%) of over 50’s say their preference would be for steady medium-long term growth if sheltered from the short-term ups and downs of the stock market. Smoothed funds can be especially helpful during periods of volatility and are well worth considering as part of the wider mix of retirement income solutions.”

|