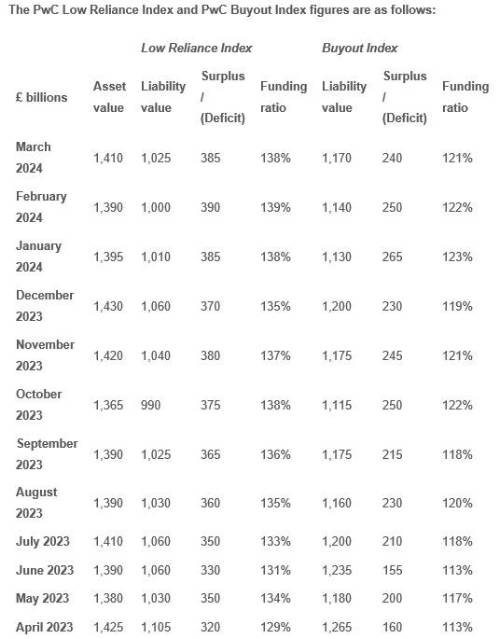

Meanwhile, PwC’s Low Reliance Index showed a near record surplus of £385bn. This index assumes schemes invest in low-risk, income-generating assets like bonds, which should mean the pension scheme is unlikely to call on the sponsor for further funding.

As a result of sustained improvements in funding levels, sponsors and trustees are increasingly re-evaluating the preferred ‘end-game’ strategies for their pension schemes.

John Dunn, head of pensions funding and transformation at PwC UK, said: “With funding levels of the UK’s DB schemes continuing to remain very strong, schemes have a significant opportunity to ‘lock-in’ improved funding positions to avoid a return to the world of deficits.

“The nature of the ‘lock’ will depend on which end-game door sponsors and trustees wish to go through - for example, to buy-out, run-on, transfer to a superfund or to alternative forms of consolidation including the proposed public sector consolidator. We are therefore supportive of the Work and Pensions Committee’s recent call for schemes to understand the potential costs and benefits of the different options before locking in.”

Alison Fleming, Chief Pensions Actuary and partner at PwC UK, added: “This mirrors the requirement from 1 April for the actuarial profession to advise their clients on the credible alternatives to particular end-game options. Pension schemes and their sponsors need to understand the benefits, cost and risks of each option as well as practical issues like timing and ease of implementation. This new requirement helps to reinforce existing actuarial standards, ensuring clients receive high quality advice in this complex area.”

|