|

|

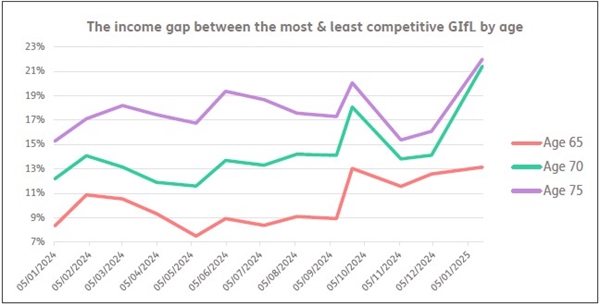

The gap between the best and worst-paying annuities has spiked higher in recent weeks, mirroring the rise in bond yields, analysis by retirement specialist Just Group of latest rates reveals. |

An annuity buyer aged 70 would secure nearly 20% more income by choosing the best deal over the worst, adding up to £7,400 more income every 10 years from a £50k pension fund. The gap at age 65 is 13%, equal to £4,380 more income over 10 years from a £50k pension. The gap has been trending higher for more than a year but has reached a peak in recent weeks. It reinforces the need for anyone considering annuities – and particularly older buyers – to ensure they shop around for the most competitive deal, potentially adding thousands to their incomes over retirement.

Stephen Lowe, group communications director at Just Group, said that it was likely that providers of Guaranteed Income for Life (GIfL) solutions were responding to movements in market rates. “GIfL pricing is influenced by the returns on gilts and bonds which have been moving up recently. It’s a competitive market and annuity providers will be watching the changes, with some responding more quickly than others depending on commercial considerations. Current annuity rates are attracting a lot of interest from retirees wanting guaranteed income but it is unlikely your own provider will pay the most. Avoiding inferior rates requires disclosing health and lifestyle information that could push the rate higher and then shopping around for the best deal.” He said all retirees should take the free, independent and impartial guidance from the government-backed Pension Wise service. Professional annuity brokers or financial advisers can help retirees choose options and scour the market for the best deal. |

|

|

|

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd