|

|

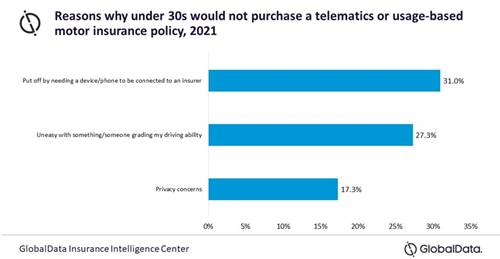

While young UK drivers have expressed various concerns around the ‘Black Box’, this has not stopped demand rising, according to GlobalData. A survey has revealed that 17.3% of under 30s highlighted privacy as an issue, while 27.3% felt uncomfortable with the idea that someone was grading their driving ability, and 31% were put off by the idea that the box had a direct line with their insurer. Despite all of these concerns, uptake of telematic devices among under 30s rose by 28.6% between 2020 and 2021. |

Benjamin Hatton, Insurance Analyst at GlobalData, comments: “Given younger consumers’ considerable online presence, it is perhaps surprising that they find the idea of data sharing and privacy to be such sticking points when it comes to telematics. Advertising the potential financial savings black boxes and usage-based products can provide may go some way to addressing these concerns. However, there also needs to be a reassurance that these services are intended to help young drivers, rather than acting as a Big Brother that’s constantly watching for errors. “Telematics can unlock discounts for good drivers, which could help young drivers who are subject to considerably greater average premiums for their car insurance. This will become especially important as the cost-of-living crisis continues.”

As the UK emerges from the COVID-19 pandemic, many consumers have considered how their driving habits and frequencies have changed.

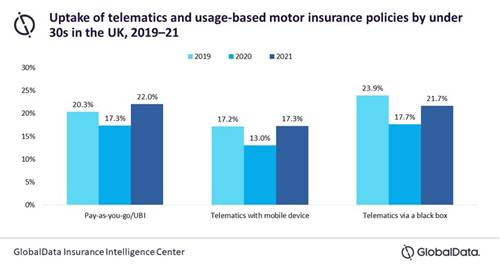

Hatton continues: “GlobalData’s survey indicates that 28.3% of under 30s believe they will be driving fewer miles annually than before the pandemic. Usage-based policies are a great way for low-milage drivers to keep their premiums low, with a growing number of young consumers looking to make use of these policies.” GlobalData forecasts a growing use of mobile devices, in lieu of black boxes, as providers increasingly enhance their digital capabilities.

Hatton adds: “The rollout of 5G networks across the UK will further facilitate mobile telematics. Moving to mobile will also remove installation costs, meaning the services are both more accessible and more affordable.” |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd