Three in seven (45%) would choose a Pot for Life if it were recommended by MoneySavingsExpert, Martin Lewis, over its financial performance (41%)

Widening financial advice gap, and low pension engagement raises concerns Brits are not fully equipped to secure a comfortable retirement

The Pots for Life call for evidence - which could see the entire UK pensions system turned upside down - did not directly include the views of pension savers. Now, research from independent consultancy Barnett Waddingham, reveals a consumer landscape conflicted; British savers are positive about this change to their pensions, but face a crisis of confidence on financial decision making.

The survey of more than 2,000 UK workers paying into a workplace DC pension reveals that over half of pension savers (53%) see Pots for Life as a positive change to the UK pension system, as many have hopes of better ways to save for their retirement. Just one in seven (15%) believe this would be a negative change. Over half (54%) said a Pot for Life would make them more engaged with their pension, and over a third (38%) said it would make them more confident about retirement.

With the Government actively considering a Lifetime Provider model in the UK, there are various benefits a Pot for Life could have for those saving for retirement, which are likely driving this positivity. Namely, it would seek to reduce the number of pots people accumulate, reducing the chances of losing pension savings in their lifetime - this being a significant problem in the UK which has seen up to 4.8 million pension pots considered ‘lost’ in 2023.

Yet, while Brits are overwhelmingly positive about Pots for Life, a clear crisis of confidence is brewing when thinking about the financial decision making required to choose a pot. Nearly half of pension savers (49%) are nervous that they would make bad decisions about which pot to choose, which rises to 53% of women and 58% of people aged 51-55 - that is, those currently likely to be planning their retirement.

This reticence in older savers plays out across pot for life positivity too - younger savers are more likely to think it would make them more engaged, with those aged 31-35 topping the list at 60% This is a stark contrast from the 44% of those closer to retirement (aged 61-65).

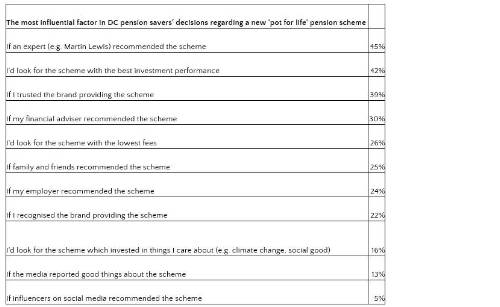

Uncertainty among savers is clearly seen in how people said they would choose a Pot for Life if they were given the option. Almost half of pension savers (45%) would trust the recommendation of consumer savings champion, Martin Lewis, over the financial performance of a fund (41%). With no clear direction on how to select a suitable pot, 39% would select a pot based on a trusted brand, or if their financial adviser were to recommend a scheme (30%), while a quarter (25%) would turn to the recommendation of friends and family.

With the FCA revealing a significant financial advice gap exists in the UK, and just 8% of of UK consumers receiving full financial advice in 2022, the results raise concern that a Pot for Life model could create a rift in the pensions market if not rolled out carefully; seeing the wealthy and confident benefitting over those with lower levels of financial means, literacy, and engagement.

Mark Futcher, Partner and Head of DC Pensions at Barnett Waddingham, said: “British savers have clearly been wooed by a sexy-sounding new pensions policy that has built up their hopes for a better future for retirement. But issues of apathy, low financial literacy, and chronically low pension saving won’t be fixed by a Pot for Life.

“What’s worse, we know that Australian SuperFunds on the other side of the world tend to splash the cash on sponsorships of sports teams, and advertising campaigns which would clearly win over savers looking for experts and brand trust. Yet, this spend comes at an opportunity cost of investing in member outcomes, and we risk a pensions system that is fighting for commercials, not consumers.

“A fresh coat of paint won’t hide the mould for long, and there are some very big pension problems the Government must fix before a Pot for Life will work. Increasing auto-enrolment levels, auto-escalating contributions at the point of pay rise, and lowering the contribution age threshold are just a few hopeful breadcrumbs. The Government must work with the industry, not against it, to create the best outcomes for pension savers. This means enacting reform to ensure the country has a financially engaged, and confident population that clearly understands their path to retirement - whatever that model may look like in ten years’ time.”

|