The spending breakdown has been graphically represented as a new Retirement Fiver to show how much those of retirement age spend on different goods and services as a proportion of £5. According to Retirement Advantage, understanding how people spend, day-to-day, has a big impact on the way in which people entering retirement plan their finances.

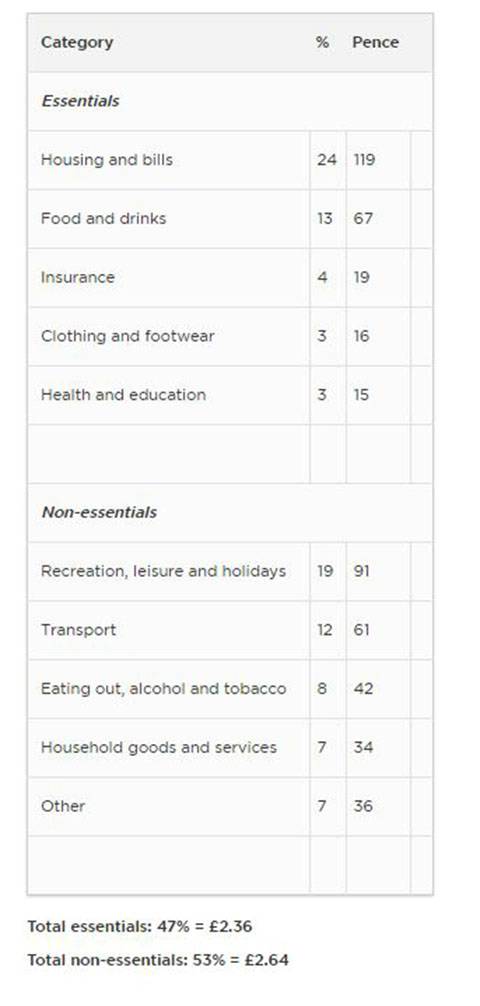

The data[1] reveals that essential elements, including housing and bills, food and drink, clothing and footwear, account for 47% of total spending, or £2.36 of a new polymer fiver. Meanwhile, non-essential products and services, such as leisure activities, holidays and eating out make up 53% of spending, or £2.64 of a fiver.

Andrew Tully, Pensions Technical Director at Retirement Advantage, comments: ‘With the new polymer five-pound note launching today, we wanted to investigate how older people really spend their money. Our analysis shows that the over 65s spend more money on what you could class non-essential elements, than they do on covering the basics such as housing, food, utilities and health.

‘It’s clear that older people want to have fun, not just survive. Our research tells us many plan to prioritise quality of life in retirement above simply making do. But to do this, retirees should be making the most of the new pension freedoms by securing an income to cover life’s basic necessities which then creates the flexibility to allow any remaining savings to grow and be used when needed to enjoy a fulfilling lifestyle.

‘To get the best possible outcome, it’s important that those approaching retirement get professional financial advice and consider how they can take advantage of new hybrid products which offer both guaranteed income to cover daily expenses and flexibility to access money for one-offs or emergencies.’

Retirement Fiver: Breakdown of spending

|