|

|

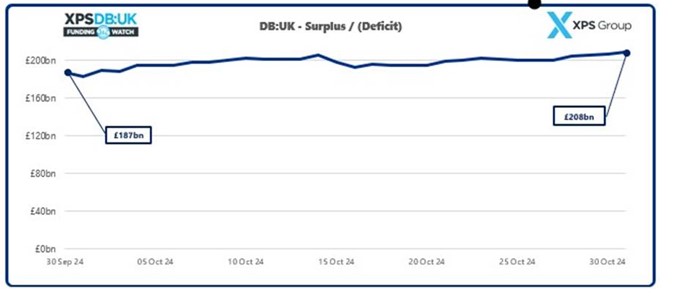

XPS Group estimates that the aggregate surplus of UK pension schemes on long-term targets remains extremely positive at ~£208bn, up significantly from £187bn in September 2024. A rise in long term gilt yields of around 0.3% led to a reduction in liability values, and improved scheme funding levels. However, this improvement was partially offset by a decline in aggregate scheme assets over the month, driven by schemes’ hedging strategies and negative returns on bonds and UK equities. |

Over October 2024, UK pension schemes’ funding positions increased significantly (relative to long-term funding targets) according to new analysis from XPS Group. With assets totalling £1,452bn and liabilities of £1,243bn, the aggregate funding level of UK pension schemes on a long-term target basis has risen to a record level, at 117% of the long-term value of liabilities, as of 31 October 2024.

The strong funding levels of many UK pension schemes improved through October in the lead up to the Labour Government’s first Budget on the 30th of October, mainly driven by rising gilt yields. Immediately following the Budget, gilt yields have continued to rise, driven by expectations of higher future government borrowing. Following the Budget, attention turned to the US presidential election result and last Thursday’s meeting of the MPC. As widely anticipated by markets, the Bank of England cut rates by 0.25% to 4.75%pa. However, rising UK government borrowing costs following the Budget, coupled with uncertainties around the global impact of Donald Trump’s re-election as US president, may cast doubts on the likelihood of further rate cuts when the MPC next meets in December

Jill Fletcher, Senior Consultant at XPS Group said: “Increases in gilt yields over October, reflecting expectations of higher government borrowing following the highly anticipated Budget, are a reminder that funding positions can change quickly. With strong surplus positions and the introduction of new DB funding regulations, many trustees and sponsors are evaluating their long-term strategies to determine whether insurance is the right route for them, or if the scheme can be used to generate additional surplus for the benefit of both members and sponsors alike. |

|

|

|

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd