|

|

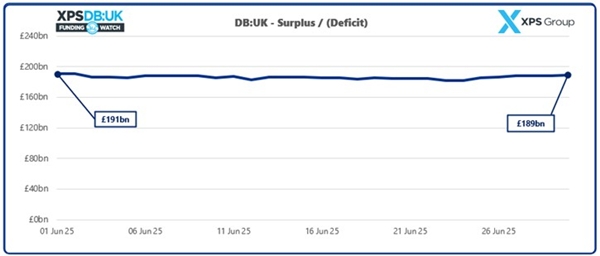

XPS Group estimates that the aggregate surplus of UK pension schemes against long-term funding targets remains extremely positive at ~£189bn, a fall of £2bn compared to the end of last month, up £26bn versus the end of June 2024. Aggregate scheme assets marginally increased over June 2025, as growth assets experienced positive returns, along with matching assets increasing in line with liabilities. Aggregate scheme liabilities increased slightly, driven by decreases in gilt yields. |

Since June 2024, UK pension schemes’ funding positions improved compared to long-term funding targets, according to new analysis from XPS Group. With assets totalling £1,151bn and liabilities of £962bn, the aggregate funding level of UK pension schemes (on a long-term funding target basis) remains extremely positive, at 120% of the long-term value of liabilities. This represents an increase of 4% over the past year, as of 30 June 2025.

Funding levels of UK DB pension schemes stayed strong over June 2025. This comes as Trustees and Employers unpacked major announcements including the Pension Schemes Bill, the Government’s response to the DWP consultation on “Options for Defined Benefit Schemes”, and guidance from the Pensions Regulator on endgame options. Trustees and Employers are now revisiting their long-term objectives and assessing what opportunities are available to them to improve outcomes for all stakeholders, as they plan how to reach their chosen endgame. For example, a recent XPS Group poll found that 76% of trustees are more likely to adopt the new statutory override to give themselves the power to distribute surplus.

Jill Fletcher, Senior Consultant at XPS Group said: “Many DB schemes are now fully funded on or above their long-term funding basis and are considering their objectives and strategy for reaching that endgame. While for some schemes the objective will continue to be working towards insuring benefits through buy-in or buy-out, the potential to run-on a scheme and make use of the recently announced surplus flexibilities may now be a more attractive and feasible option for others.” |

|

|

|

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd