|

|

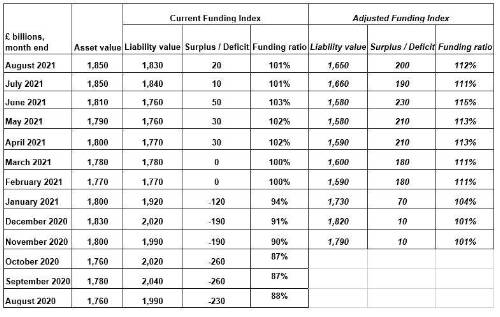

The funding status for the UK’s 5,300 corporate defined benefit (DB) pension schemes remained relatively stable over August according to the PwC Pension Funding Index, with the Current Funding Index showing an aggregate surplus and the Adjusted Funding Index continuing to show a significant surplus. unding position for UK defined benefit pension schemes remains relatively stable over Augus |

Liability values fell slightly over August while asset values remained stable. As a result the overall funding position continues to show a surplus of £20bn based on schemes’ own measures, while PwC’s Adjusted Funding Index continues to show a sizable surplus of £200bn. The PwC Adjusted Funding Index takes into account available strategies such as switching from low-yielding gilt investments to higher-return, income-generating assets. It also takes a more realistic approach to life expectancy changes. Emma Morton, pensions actuary at PwC, said: “A significant number of pension schemes are now in surplus. This is evident from our analysis of the aggregate funding position. “While it’s right that sponsors and trustees should fund their schemes prudently, it’s important not to be too prudent. Once a scheme is in surplus, it is difficult for the sponsor to get that money back, even once all the scheme’s benefits have been secured. “Over-funding schemes isn’t necessarily in trustees’ or members’ best interests, either. Scheme rules often don’t make it clear how a surplus should be spent, and it can be a dilemma for trustees to decide whether to use a surplus to increase members’ benefits or return it to the sponsor - particularly if the sponsor can ill afford to write this money off. Refunds of surplus are also subject to a 35% tax charge. “It's far more common for sponsors to pay money into a scheme, than it is to get that money back. Sponsors and trustees should keep this asymmetry in mind when funding schemes. If the valuation was carried out at a date when markets made the funding position look particularly bad, and the funding position has since improved, these improvements should be taken into account when deciding how much cash the sponsor should pay into the scheme.”

The PwC Pension Funding Index and PwC Adjusted Funding Index figures are as follows: |

|

|

|

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd