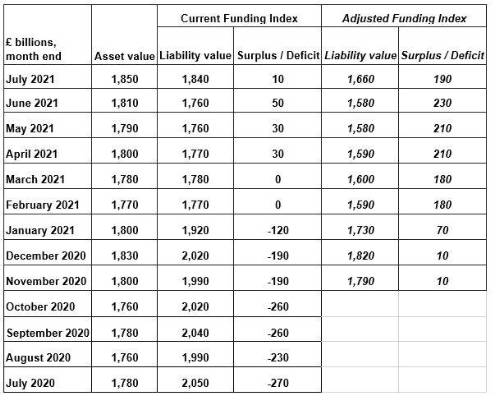

Liability values increased by £80bn over July, driven by falling gilt yields. Asset values have also increased to offset some of this, and as a result the overall funding position continues to show a surplus of £10bn based on schemes’ own measures. This now makes for six months of aggregate surplus for the UKs DB scheme universe.

PwC’s Adjusted Funding Index showed a £190bn surplus. This incorporates strategic changes available for most pension funds, including a move away from low-yielding gilt investments to higher-return, income-generating assets. It also uses a different, more realistic approach for the longevity assumption. This is an area sponsors and trustees might want to pay particular attention to. The Pensions Regulator (tPR) also noted in their recent Annual Funding Statement that assumptions for life expectancy would need careful consideration, as a result of the uncertainty that Covid-19 brings. In their Statement, tPR suggests that one way to deal with this uncertainty might be to retain an assumption similar to previous valuations and let any positive experience unfold over future valuations.

Raj Mody partner and global head of pensions at PwC, said: “It might sound easier for schemes to leave the longevity assumption unchanged at their next valuation, but it could do more harm than good.

“Long-term life expectancies have always been hard to predict, and schemes make estimates using the most up-to-date information they have. Keeping the same longevity assumption would mean not taking into account the latest data. It is better for schemes to reassess their longevity assumptions based on the latest evidence available - modern analytical tools and techniques allow this.

“Where part of the assumptions relate to future long-term forecasting and where it’s as much an estimate as informed by data, it’s even more important not to settle for ‘what you did last time’. If trustees and sponsors approached all their actuarial assumptions like that, then pension scheme strategies would end up wildly out of kilter with real-life needs. It’s crucial to make the most informed decision you can at any given time.

“The risk with just sticking with old forecasts is that it could require excess money being paid irreversibly into schemes in the short term, to fund prospective life expectancy improvements which are decades out and may not even happen. This might be appropriate for some schemes, but it’s unlikely to be right for the majority.”

The PwC Pension Funding Index and PwC Adjusted Funding Index figures are as follows:

|