However, total premium volumes will return to pre-crisis levels in 2021 already, alongside more protracted recovery in the global economy. There will be sector divergence, with non-life premium volumes above pre-crisis levels, and life below. The emerging economies, led by China, will underpin the insurance market comeback.

"The insurance industry is showing resilience in face of the COVID-19-led economic downturn," Jerome Jean Haegeli, Group Chief Economist at Swiss Re said. "The magnitude of premium losses will be similar to that seen during the global financial crisis in 2008-09, even though this year's economic contraction of around 4% will be much more severe. Unlike for the global economy, we expect a strong V-shaped recovery in insurance premiums, a remarkable showing considering that the world is currently in the throes of the deepest recession ever".

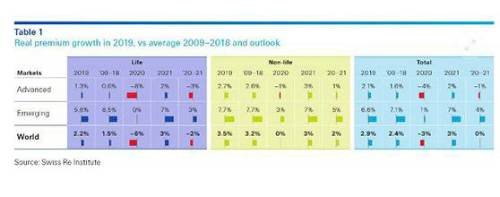

This year's recession will be the deepest since the Great Depression of the 1930s, but it will also be short-lived. The recession will lead to a steep fall in demand for insurance. After growing by 2.2% in 2019, global life premiums are forecast to contract by 6% in 2020. Due to prevailing and lower interest rates, savings products will be more affected, while mortality related covers will be more stable. The non-life sector will fare better, with global premiums forecast to be broadly flat (-0.1%) after growing by 3.5% in 2019. A main reason for the better showing in non-life is that the COVID-19 crisis has hit at a time of rate hardening in the sector, which has supported premium growth. Premiums in trade and travel-related insurance business such as marine, aviation and credit will be hit the hardest. Property and medical business will be more stable.

Emerging Asia, led by China, to underpin market resilience through 2021

Swiss Re Institute estimates that total premium volumes in advanced markets (life and non-life) will shrink by 4% this year and return to positive growth of more than 2% in 2021. In the emerging markets, premium growth will remain in positive territory in both years, up 1% in 2020 and 7% in 2021.

Insurance industry will absorb the earnings shock

There is exceptional uncertainty about what the ultimate claims burden from the pandemic will be, with the mid-point of the range of current estimates from various external and public sources at around USD 55 billion. The insurance industry is very well capitalised to absorb losses.

"The industry's capital position means it should be able to handle the COVID-19 shock. The upper end of the range of total property and casualty claims estimates by most external insurance analysis is USD 100 billion, similar in scale to losses caused by Hurricanes Harvey, Irma and Maria in 2017, which the industry also absorbed," Haegeli said.

"The COVID-19 experience highlights the importance of insurance provision for pandemics. It is a lesson for insurers and policy makers alike who, in the interest of long-term societal and economic stability, should look to develop more public-private partnership solutions for pandemic risks".

The COVID-19 crisis will present challenges to industry profitability. In addition to pandemic-related losses, investment returns will remain subdued as interest rates stay low for longer, impacting life and long-tail lines in non-life. Rising corporate defaults could lead to losses on invested assets. In life, claims payments due to COVID-19 will likely have limited impact, but falling sales and fee income due to restricted in-person interactions on account of the lockdown measures imposed to contain the spread of the coronavirus, will weigh on profits this year.

On the flipside, COVID-19 has hit at a time of rate hardening in non-life, a trend that is likely to continue amid potentially high losses and contracting insurance supply, particularly in commercial lines. This, and the expected bounce-back of insurance demand, will support earnings over the longer term. The experience of this year's health and economic crises will raise risk awareness and demand for risk protection across many lines of business. The COVID-19 shock will likely accelerate other paradigm shifts too, such as a restructuring of global supply chains to mitigate future business disruption risks, giving rise to new premium pools in property, engineering and surety insurance.

|