Isio has published its latest analysis of the investment performance and asset allocation of 14 major UK DC master trust providers. The latest quarterly update highlights how providers are continuing to position members for long-term growth despite a more volatile market backdrop in Q1 2026.

Global equities declined over the quarter amid heightened geopolitical uncertainty and rising energy prices, with US equities particularly weak as technology stocks retraced following strong performance in 2025. Emerging markets proved more resilient, while UK equities delivered positive returns supported by higher oil prices and a weaker sterling.

At the same time, rising inflation expectations pushed gilt yields higher, weighing on conventional bonds, while credit markets also delivered negative returns. Despite this more challenging environment, the quarter reinforced a broader structural trend across the DC market: providers are increasingly prioritising long-term retirement outcomes over short-term stability.

Providers maintain long-term focus through market volatility

Periods of short-term volatility remain an expected feature of long-term investing, particularly for growth phase strategies with higher exposure to equities and other return-seeking assets.

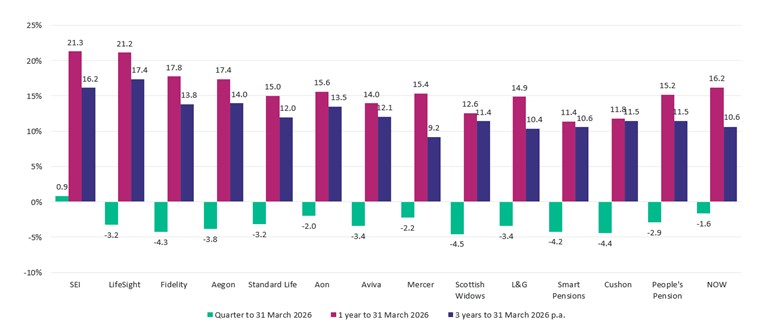

Across the provider landscape, growth phase strategies experienced a wide dispersion of returns over Q1, ranging from +0.9% to -4.5%, reflecting differences in equity exposure, regional positioning and overall strategy design. However, longer-term outcomes remained significantly stronger, with three-year annualised returns ranging from 9.2% p.a. to 17.4% p.a. However, recent changes to many strategies mean historic performance should be interpreted with caution.

Performance to 31 March 2026 - Growth Phase (30 years to retirement)

The variation in outcomes highlights the increasing importance of strategic design decisions within default strategies. While equity allocations have been a key driver of returns in recent years, providers are also gradually introducing private market exposures and broadening diversification, which could lead to greater differentiation between strategies over time.

Importantly, providers continue to maintain a long-term approach despite periods of market stress. Recent member behaviour during episodes such as the Covid pandemic and tariff-driven volatility in 2025 has shown limited evidence of panic-driven disinvestment, supporting greater confidence in maintaining exposure to growth assets where appropriate.

Retirement strategies continue evolving beyond traditional de-risking

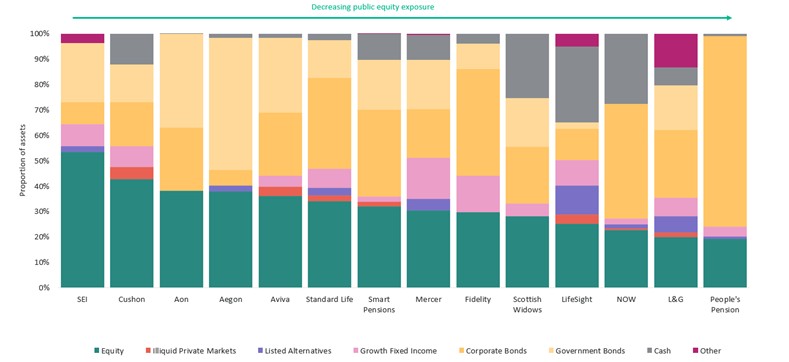

The evolution in at-retirement strategy design also continued through Q1. While most at-retirement strategies delivered modest negative returns over the quarter, the narrower range of outcomes compared to the growth phase demonstrated the benefits of diversification in helping manage downside risk. Importantly, maintaining exposure to equities did not necessarily result in materially worse outcomes during the period.

Providers are increasingly designing retirement strategies to reflect longer retirement horizons and growing use of drawdown rather than focusing solely on capital preservation or annuity purchase.

At Retirement Phase - Peer Group Asset Allocation (0 years to retirement)

This has led to a gradual shift toward retaining growth assets for longer, alongside broader diversification across fixed income and alternative credit assets. The move reflects increasing industry recognition that excessive early de-risking can raise the risk of inadequate retirement income over the long term.

Alongside this, providers are continuing to develop more holistic post-retirement solutions, including guided retirement approaches designed to support members as they transition from accumulation into decumulation.

Mark Powley, Head of DC Master Trust Research at Isio, said: “Q1 was a reminder that periods of volatility are a normal part of long-term investing, particularly following a sustained period of strong market performance. What’s notable is that providers have generally maintained a disciplined long-term approach rather than reacting to short-term market movements.

"We continue to see strategies evolving to reflect changing retirement behaviours and the growing recognition that more members are likely to remain invested for longer into retirement. That is leading providers to retain growth assets for longer, while also broadening diversification to help manage downside risk more effectively.

“The increasing dispersion in returns also highlights how important strategic design decisions are becoming across the DC market. As private market allocations continue to develop and retirement solutions evolve further, we expect differentiation between strategies to become even more pronounced over time.”

|