|

|

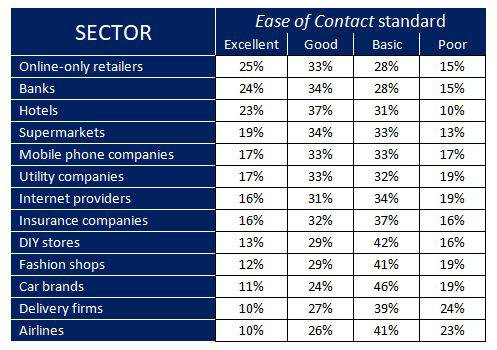

Insurance companies are failing to offer premium levels of contactability to their customers and prospects, according to the findings of latest research. This oversight is particularly astonishing in today’s connected world, where reputations are made and lost on internet reviews and competition across channels is increasingly fierce. |

The research commissioned by Yonder Digital Group canvassed 2,000 UK consumers, asking whether they felt that companies in a range of sectors were easy to get in touch with and efficient at getting queries resolved rapidly and effectively. Today’s consumers are in fact increasingly accustomed to swift query response, across multiple channels, but the research results show that many sectors are failing to meet these taxing demands.

In relation to other sectors, insurance companies sit in the middle with 16% of consumers surveyed scoring the sector excellent and 32% ‘good’ for ease of contact. This leaves just over half of consumers who rated insurers as ‘basic’ or ‘poor’, hardly acceptable considering that insurers are one of the first ports of call after accidents and in moments of crisis. With previous Yonder research showing that 81% of consumers simply take their business elsewhere if their queries aren't answered quickly and effectively by a company, it is highly risky for insurance businesses to continue overlooking their levels of ‘contactability’. Chris Robinson, Yonder Digital Group CEO, comments, “Customers have individual preferences for contacting companies, which is why businesses lose out when they don’t offer a range of touch points. At crucial moments in the journey to purchase, many customers will look for a live agent, particularly for urgent or non-standard queries. Businesses that fail to provide support at these critical stages risk losing customers to competitors with superior support services. As the results show, a large proportion of companies are still falling well below the mark, suggesting there is a long way to go for UK industries to catch up with modern expectations.” |

|

|

|

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd