LCP attributes this to record insurer capacity exceeding short-term demand and a growing contribution from newer insurer entrants, increasing competition for transactions of all sizes.

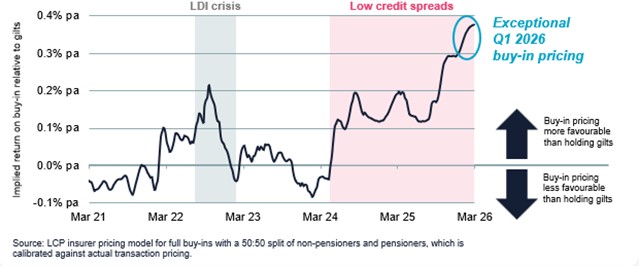

Buy-in pricing reached its most competitive levels yet in Q1 2026, as shown in the chart below. Pricing has remained broadly unaffected by the recent market turmoil stemming from the conflict in the Middle East, with attractive pricing continuing into Q2 2026 and many LCP clients securing even better pricing than was available in Q1 2026.

Buy-in pricing relative to yields available on gilts

Total buy-in volumes reached £38.2bn in 2025. Looking forward, volumes in 2026 will depend on whether certain £1bn+ buy-ins transact this year or next. LCP expects another year of high activity but not record volumes, meaning that insurer capacity should more than meet demand, with high competition continuing for the rest of the year.

Newer insurer entrants are contributing to the market's momentum. Royal London, Prudential and Utmost consolidated their presence, with their combined market share growing to 9% of volumes in 2025, up from only 3% in 2024. Together with Blumont*, they completed £3.4bn across 46 transactions in 2025 – a significant increase on the £1.5bn across nine transactions in 2024. This contributed to more than half of the growth in transaction numbers (up 23% from 298 in 2024 to 367 in 2025).

Schemes are placing greater focus on non-price factors, with insurers’ member offerings now a key differentiator. The landmark Rolls Royce transaction, which placed member outcomes at its core, is a clear example of this shift. Insurers are enhancing the member experience through innovations such as online benefit modellers and end to end self service retirement journeys. At the same time, increased automation and more streamlined operating models are helping insurers to deliver faster, more efficient retirement quotations and improved support for member interactions, which is helping to ease recent delivery bottlenecks for some insurers.

Smaller schemes below £100m are benefiting from current market dynamics and account for a growing share of the market (83% by number in 2025 compared to 54% five years ago). With increased insurer participation and fewer larger transactions in 2025 (and expected in 2026), this once under-served segment is now flourishing. All insurers wrote sub-£100m transactions in 2025, with insurers’ streamlined offerings supporting expanded capacity to quote.

Charlie Finch, Partner at LCP, said: “Twenty years on from the first buy-in, the UK pension risk transfer market is seeing record levels of competition and choice. Strong insurer capacity and heightened competition have driven the attractiveness of buy-in pricing for LCP clients to unprecedented levels in early 2026.

“For well-prepared schemes, the current market presents a compelling pricing opportunity and gives leverage to negotiate bespoke terms for the benefit of members.”

Ruth Ward, Partner at LCP, added: “Competition is no longer limited to the largest transactions, with smaller schemes benefiting from a wider range of insurers actively participating in this segment and improved access to the market. For trustees and sponsors, that creates a real opportunity.

“Whilst market conditions are favourable, it’s important not to lose sight of the fact that hundreds of schemes are now seeking buy-in quotations. Good quality preparation is therefore critical to stand out from the crowd, achieve strong insurer engagement and ensure efficient post-transaction processes.”

|