A month on, we seem to be stumbling towards a resolution in which transit through the Strait of Hormuz will be possible again. This is very much a two-steps-forward, one-step-backward process, and of course (at the time of writing) risks of a complete breakdown in negotiations remain. But we believe it is now time to start anticipating a post-resolution investment landscape.

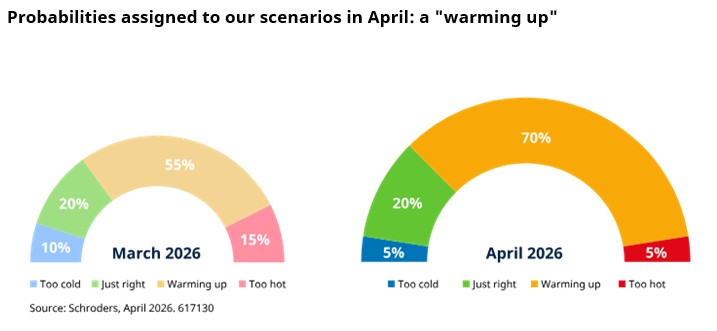

Our scenario probabilities reflect these changes. The war and energy shock raised the tail risks on both sides – though by more on the "too hot" front – and so the path towards resolution sees us reduce these, with “warming up” remaining our modal expectation.

Source: Schroders Global Unconstrained Fixed Income team 20 April 2026, for illustrative purposes only. The “‘too cold”’ scenario would see the Federal Reserve (Fed) cutting 4+ times in 2026, 2-3 cuts for “‘just right”’, while in “‘warming up”’ the Fed is only cutting once or is on hold. Finally, in a “‘too hot”’ scenario the Fed is moving back towards hikes in 2026, because inflation is becoming problematic again.

Push meets pull

At this stage – with only limited data about the full impact of the war on growth – our base case for the US economy is that it will be a manageable headwind. This is because of the underlying strength from consumers and the manufacturing cycle going into this. We’re also seeing continued signs that the labour market has based and is improving.

For sure, consumer real incomes (incomes adjusted for inflation) will be dented by rising oil prices. We expect a peak impact on inflation of about 1% above the previous baseline, but other factors are offsetting this. The consumer elements of One Big Beautiful Bill (OBBB) are kicking in, with income tax refunds largely offsetting the drag of higher gasoline prices at the pump. These opposing forces means in aggregate US consumers will end up in largely the same place.

A reduction in customs duties over recent months, in part due to the Supreme Court ruling against IEEPA tariffs (those tariffs implemented by use of the Internation Emergency Economic Powers Act) should also lead – at a minimum – to a slower rise in goods prices. Again, supporting real incomes.

Eurozone growth should also muddle though

The eurozone is doubly impacted by the closure of the Strait of Hormuz due to the impact on natural gas prices, crucial for electricity and heating. Though the initial reaction to the war was sharp, gas prices have retraced a significant portion of this move, leaving them elevated relative to their pre-war baseline but still significantly lower than after the Russia/Ukraine conflict in 2022.

We expect that the impact on the eurozone economy will be noticeable, but not recessionary. Like the US, this is partly a function of a solid starting point with the region’s cyclical dynamics providing a resilience to the economy.

The European Central Bank (ECB) has so far taken a non-committal approach, but will be attentive to rising headline inflation. We expect them to be among the more hawkish of central banks, and while this doesn't guarantee rate increases or rule out eurozone bond rallies if energy prices drop sharply, overall, we find better risk-reward elsewhere, such as in Canada, Australia, and the UK.

Early signs of fuel shortages impacting Asian economies

Asia faces the greatest economic risk from energy shortages if the Strait of Hormuz is not reopened. In fact, we can already see a clear distinction between those Asian economies most and least exposed to energy shortages in the latest set of Purchasing Manager Index releases (PMIs). At this stage, the economic disruption is limited and largely reversible if we see a quick resumption of supplies supported by a trade cycle – especially linked to tech and semiconductors – which was improving before the war.

Upgrades aplenty

So as we begin to position for a post-resolution world, albeit with a bumpy path likely, where do we want exposure? We upgrade our overall score on global duration (interest rate risk) to positive from neutral, given our expectation that the peak impact from energy prices is behind us. We continue to see the best opportunities in Canada, Australia and shorter-maturity UK gilts, while turning neutral on US treasuries (previously negative). We remain neutral on German bunds.

In asset allocation, we move back to a negative stance on both high yield and investment grade credit given unattractive valuations. Having moved wider during March, spreads (the premium over government bonds) have been quick to retrace back to levels similar to the onset of the Iranian conflict. For similar reasons, we downgrade US agency mortgage-backed securities back to a neutral score. Scores in emerging market debt are positive.

|