Profile Pensions have analysed the monthly spending habits of Millennials, from necessary living expenses, to flat whites and takeaways, to help illustrate to Millennials their financial state if they don’t at least start thinking about retirement now.

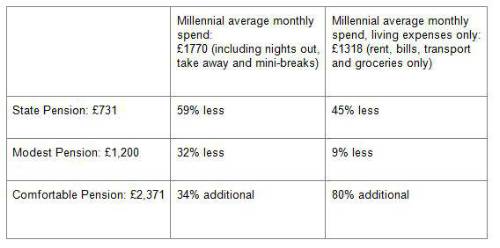

How Much Less Will it Really be?

Top Saving Tips

• Take Advantage of Pension Schemes - All workplaces should offer a pension scheme, committing to this means that a portion of your salary (commonly 5%) is dedicated towards retirement for you.

• Cut Back On Big Nights - On average, the research found we spend £211 on a night out - that’s 32% of the state pension. If we cut that in half we could put that extra £100 into a private pension.

• Eat More, Takeaway Less - Combining the average amount spent on groceries and takeaways equals £300 a month. Cutting back on just takeaways can save an extra £80 each month towards your pension.

Michelle Gribbin, Chief Investment Officer at Profile Pensions commented, “Although monthly expenses can vary from generation to generation, we wanted to showcase to those still climbing the career ladder the necessity of preparing for their financial future early, by highlighting just how much of their current lifestyles they would have to change in order to live comfortably in retirement. Although it can be easy to glance over small indulgences from time to time, it does all add up, and preparing for retirement is key for us all, no matter our age. In fact, as our results show, the earlier you can start saving, the more comfortable your retirement can be. ”

Uncover more about how a Millennial lifestyle translates to a pensioner’s budget, and tips on how to ensure you’re prepared.

|