|

|

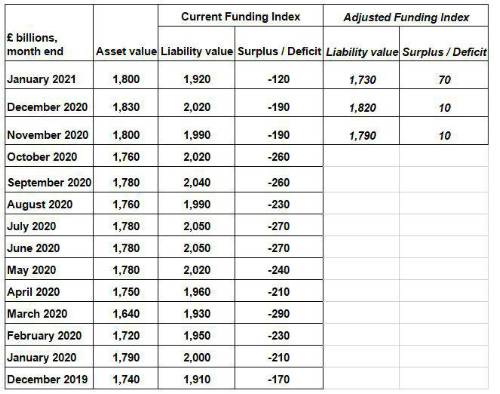

The funding deficit for the UK’s 5,000-plus corporate defined benefit (DB) pension schemes fell to £120bn in January, according to schemes’ own measures, while PwC analysis shows how a new approach to funding could leave schemes with a £70bn surplus. |

Pension fund assets and liability values both fell in January, measured on the funding assumptions which pension schemes are currently using. The net result of a £120bn deficit is lower than levels seen during the course of 2020, reflecting a recovery in asset values since the market shocks of 2020. Raj Mody, global head of pensions at PwC, said: “2020 was a turbulent year for geopolitics, the economy and the country as a whole, full of uncertainty for both markets and individuals. The last couple of months of the year showed signs of improvement for pension schemes financial health, which has sustained into early 2021.” PwC recently introduced a new Adjusted Funding Index, which shows a DB pension scheme surplus of £70bn for January 2021. The Adjusted Funding approach incorporates strategic changes available for most pension schemes, including a move away from gilt investments to higher-return, cash flow generative assets, along with a new approach for funding long-term potential life expectancy improvements which are yet to happen. Raj Mody added: “The Adjusted Funding Index shows what the funding position would be if trustees and sponsors made various changes to their investment and funding strategies. Current approaches to pension scheme management may be out-of-date, having been created in different conditions. Innovation in markets allows pension schemes to access new opportunities, as they continue to mature and the profile of their obligations changes. Deploying these techniques would wipe out the aggregate deficit in defined benefit pension schemes, allowing sponsoring companies to reinvest spare cash in their businesses, new jobs and the wider economic recovery.” The PwC Pension Funding Index and PwC Adjusted Funding Index figures are as follows:

|

|

|

|

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd