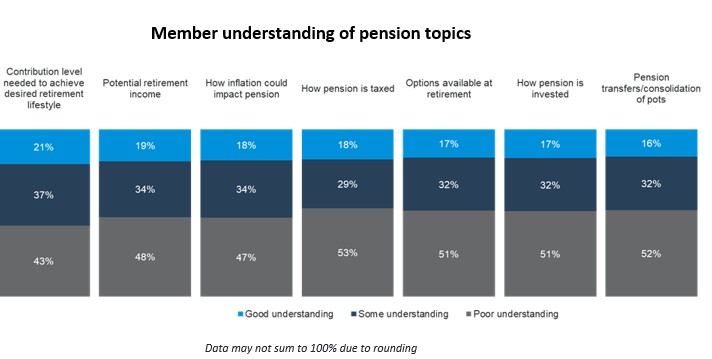

A CoreData survey of 3,000 UK DC pension members found glaring gaps in knowledge across a range of essential pension areas. Only one in five respondents say they have a good understanding of their potential retirement income (19%) and the contribution levels needed to achieve desired retirement lifestyles (21%). Even fewer report good understanding of consolidating DC pots (16%), options available at retirement (17%) and how their pension is invested (17%) and taxed (18%).

Knowledge gaps are wider for those on low incomes. Just one in 10 members with incomes less than £25,000 have a good grasp of how their pension is invested (10%) and what overall retirement income they are on course to achieve (14%).

The survey, conducted in Q4 2025, also shows how these knowledge gaps are translating into a lack of meaningful action. About two-thirds of members have never changed how their pension is invested (68%) and never consolidated their DC pension pots (66%). In addition, more than half have never set a specific retirement date (62%) or increased monthly pension contributions (55%).

Despite these knowledge and action gaps, the study highlights relatively high levels of digital interaction with DC providers. A majority (55%) of members have used their provider’s online portal to check or manage their pension within the last 12 months, while 39% have used their provider’s mobile app. And 57% say they view their main provider’s website or mobile app as a key source of information and educational content.

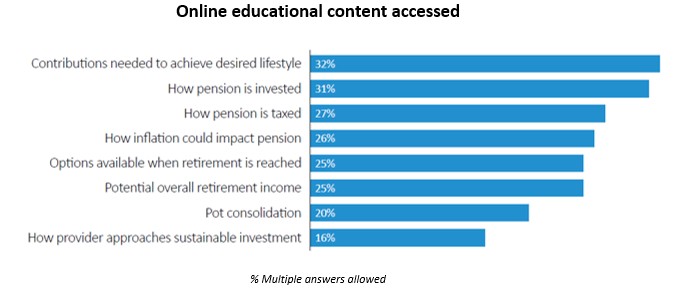

While members see their provider’s digital channels as a vital information hub, most are not making use of the educational content provided. Less than a third have accessed online information on core areas including contributions needed to achieve their desired retirement lifestyle (32%), how inflation impacts pensions (26%), options available upon retirement (25%) and potential overall retirement income (25%).

A key focus of the study was to understand how more tailored approaches to member engagement – utilising digital channels – may help to drive more positive pension behaviours.

“Encouragingly, our findings show that a growing number of members across all age groups are now visiting their pension providers’ digital channels. But on the flipside, we see that this interaction is not translating into engagement that boosts member understanding and ultimately spurs meaningful action,” says Joe Dalton, Head of Research, Europe, at CoreData.

The research also assessed how the barriers to taking pension actions differ for members within different age cohorts, income levels and of differing financial literacy levels. “Our analysis highlights how financial literacy, life stage and wealth levels all affect not just the type of information needed by different members to support better decisions, but also the way in which that information is delivered,” adds Dalton.

“Some cohorts are avoiding engagement with their pension because they’re afraid of what they might find, others are eager to take action but struggle to understand what income they will need and what their current trajectory is – and then there are more complacent members who think they’ll be fine because they are making the minimum auto-enrolment contributions.”

“Given these different factors, a one-size-fits-all approach to member engagement is unlikely to drive the necessary behavioural change to meaningfully improve retirement outcomes. A more tailored approach to engagement is needed, and that requires building a more complete picture of individual members’ financial situation and behavioural profile and harnessing technology to deliver tailored communication at scale.”

Key Findings

|