|

|

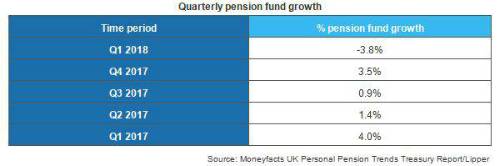

New data from the latest Moneyfacts UK Personal Pension Trends Treasury Report has revealed deteriorating pension fund performance in Q1 2018 at a time when members of auto-enrolment schemes are seeing their mandatory minimum contribution rates rise from 1% to 3%. |

The report shows how after a run of positive gains in the previous nine quarters the average pension fund registered a loss for the first time since Q3 2015, falling by 3.8%. Of the 36 ABI pension fund sectors surveyed, only two (UK Direct Property and Money Market) avoided a fall. The heaviest losses during the quarter were suffered by Commodity/Energy (-10.4%), Global Property (-6.8%) and UK All?Companies (-6.1%). The extent of the more difficult conditions for pension funds in Q1 2018 can be seen by the fact that only 7% of all the pension funds surveyed produced growth during this period.

Pension fund performance is likely to be more prominent in the minds of those saving into a workplace pension now that the Government’s first phase of its increase to minimum contribution rates for auto-enrolment is underway. Mandatory contribution rates rose to a combined 5% from 6 April 2018, of which at least 3% must come from the employee. The minimum contribution level will rise further to 8% in April 2019, of which 5% must come from the employee. Richard Eagling, Head of Pensions at Moneyfacts, said: “A major concern is how employees will react to seeing their minimum pension contributions triple. With signs of greater volatility returning to the investment markets it will be interesting to see if this dampens enthusiasm for saving into a personal pension or workplace pension, particularly given the higher minimum contribution rates that employees are now facing. It could also encourage individuals to reconsider their retirement income decisions at the decumulation stage by favouring the secure income of an annuity over the greater flexibility and risks inherent in drawdown.” |

|

|

|

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd