|

|

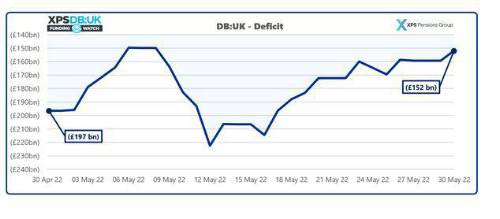

UK pension scheme deficits against long-term funding targets fell by £45bn over the month to May 20221, driven by rising gilt yields and a fall in long term inflation expectations. DB:UK estimates that it will currently take less than 4 years2 to reach long-term targets under the proposed new funding code rules. |

Deficits of UK pension schemes have decreased by c.£45bn over the month to 30 May 2022 against long-term funding targets, an analysis from XPS’s DB:UK funding tracker has revealed. The 25% reduction was primarily driven by a further rise in gilts yields as well as a fall in long term inflation expectations. Based on assets of £1,689bn and liabilities of £1,841bn, the average funding level of UK pension schemes on a long-term target basis was 91.8% as of 30 May 2022. XPS estimates that at the end of May 2022 the average pension scheme would need an additional £15,000 per member to ensure it can pay their pensions into the long-term.

Drivers of the change

Funding levels over May were volatile. Liabilities fell due to rising gilt yields and lower expectations of long-term inflation. Despite ongoing concerns about short term inflation and the rising cost of living, long-term inflation expectations fell over the month helping to reduce deficits further.

Charlotte Jones, Senior Consultant at XPS Pensions Group said: “Despite improvement in schemes’ positions over May, it was a volatile month. Short term inflation reached a 40-year high, gilt yields fell and subsequently rose again by 0.30% and schemes’ assets suffered similar volatility due to continued economic concerns across global markets. This uncertainty highlights the need for schemes to keep on top of their hedging arrangements, particularly considering the recent inflation hikes. However, despite such volatility some schemes will be in a good position and looking to reach their long-term targets within 4 years meaning that it is becoming increasingly important for schemes to prepare ahead of their conclusion.” |

|

|

|

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd