|

|

Alliance Trust Savings have published research that has found a serious lack of awareness of administration charges among people saving into workplace or personal pensions with just over a quarter (27%) believing they do not pay any administration fees for their investments. |

The nationwide survey of 1,000 individuals regularly investing into at least one investment product (workplace pension, personal pension, stocks and shares ISA, general investing accounts or investment fund) also revealed that among pension savers who said they pay an administration fee for their investment, more than two thirds (68%) do not know how much it was. Women and the over 45s were least likely to know, with three quarters of each group (75% and 74% respectively) admitting to not being aware of the costs of their investment. Almost two out of five (38%) knew whether they pay a flat fee or a percentage fee for their pension or investment.

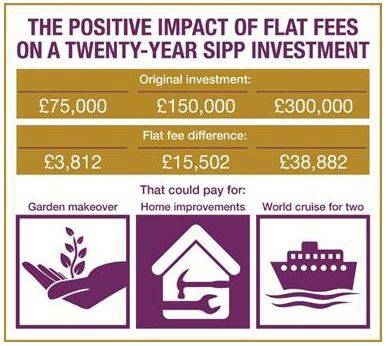

With a set, flat fee, everyone pays the same. For people with larger accounts, flat fees can offer excellent value and make a big difference to what you could get back over the longer term. A £150,000 pension pot could be more than £15,000 bigger after 20 years, just by paying a flat platform fee rather than a percentage fee. Sara Wilson, Head of Platform Proposition at Alliance Trust Savings, commented: “Fees can make a huge difference to the value of a pension pot over time. Whether you pay flat fees or percentage fees for your platform administration can also impact your investment returns significantly over a twenty-year period. Many platforms charge a percentage fee, but the reality is that it does not cost ten times as much to service a £500,000 pension as it does to service a £50,000 one. For people with larger accounts, flat fees can offer excellent value and make a big difference to what you could get back over the longer term.” |

|

|

|

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd