Sarah Abraham, Head of Redress Services at First Actuarial, explains: “When we calculate redress for someone who has transferred a DB pension into a Defined Contribution pension arrangement, we compare the amount of money the consumer holds in their new pension with the cost of buying an annuity to broadly replicate the DB pension they gave up. Gilt yields are a key driver for annuity prices – the cost of buying an annuity falls as yields increase. This makes the yields available on gilts a key driver of the size of redress payments.”

Since July 2025, investment returns on equities and other growth assets have shown a positive trajectory. This has also had a favourable effect on redress payments.

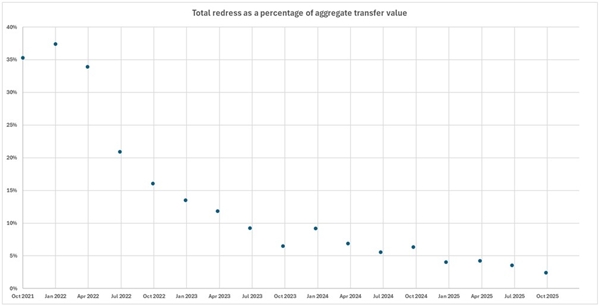

Sarah continues: “Under FCA rules, redress offers made before 31 December 2025 will reflect market conditions at 1 October 2025. We expect redress payments to be lower than we’ve ever seen before, with many cases requiring no compensation at all. This is good news for those firms that are able to settle this quarter on complaints about DB pension transfer advice or recommendations to public service workers who may have chosen to set up freestanding AVCs rather than purchase additional DB pension.”

First Actuarial Redress Tracker as at 1 October 2025

The First Actuarial Redress Tracker models the aggregate redress for a portfolio of notional cases. The notional portfolio reflects redress in relation to transfers from a variety of schemes, with a range of transfer dates and consumer ages. Allowance is made for transfer proceeds to have been invested in a mixed portfolio of assets.

|