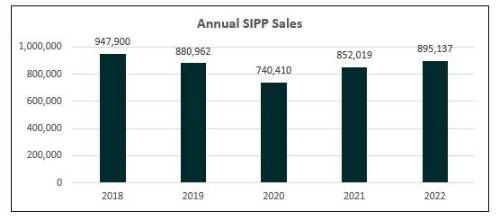

Sales of self-invested personal pensions (SIPPs) recorded a second consecutive year of growth following a downturn during the pandemic, reveals the analysis of the latest FCA data by Broadstone.

After falling to 740,410 in 2020, sales increased by 15% to 852,019 in 2021 and then by a further 5% annualised to reach 895,137 in 2022.

It marks the highest annual total of SIPP sales since 2018 when 947,900 were sold. On a quarterly basis, Q1 2022 saw 240,903 SIPP sales – the highest total since Q4 2018 (240,940).

A SIPP is a type of defined contribution pension plan which enjoys the same tax benefits as other types of pension arrangements but gives the saver greater choice over how and where their money is invested. There are now a wide variety of products to choose from, ranging from ‘full’ advised SIPPs through ready-made portfolio providers to so-called ‘DIY’ SIPPs.

Damon Hopkins, Head of DC Workplace Savings at Broadstone, said, “For pension savers with the time and know-how to navigate the world of investments, SIPPs are a good way to exercise greater control over their pension.

“In that context, the growth in sales of self-invested personal pensions suggests that savers are becoming increasingly confident in managing their own finances – particularly given the rocky macro-economic environment we are experiencing.

“Greater engagement and participation in pension savings is ultimately what all industry stakeholders are aiming to achieve, so these examples of green shoots are encouraging. However, the challenge of achieving retirement adequacy through DC across the entire population remains a very significant one.”

|