Jack Carmichael, Associate and Senior Consulting Actuary at Barnett Waddingham, comments: "There is a very real risk that the OBR's analysis of the future cost of the State Pension actually doesn't go far enough to illustrate how much longevity risk the current system poses to the UK's public finances. The OBR's "Fiscal risks and sustainability" report shows the cost of State Pension as a proportion of GDP doubling over the next 50 years, driven by a growing retirement population relative to the working age population.

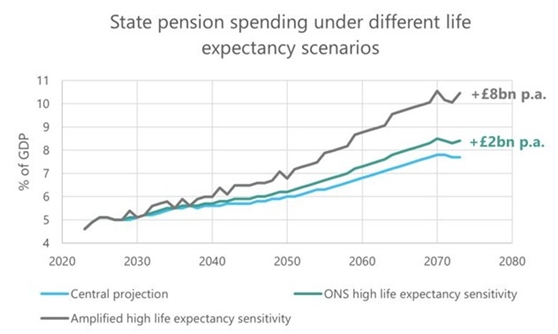

"The OBR's modelling uses a high life expectancy scenario, based on the ONS's definition in their population projections, that results in an additional annual State Pension cost of c. £2bn in today's terms. It assumes a long-term rate of 1.9%, rather than 1.2%. In reality, that sensitivity is too cautious and broad-brush, which underplays the degree of longevity risk in the State Pension system. A more cautious approach would be to assume a closing of the life expectancy gap between the individuals with the lowest and highest life expectancy. Not only does this more accurately capture the financial impact of longevity risk in the UK State Pension system, it is also more likely to reflect healthcare spending priorities over the next 50 years if those living the longest at the moment are assumed to have almost reached the life expectancy cap.

"Under this alternative life expectancy sensitivity, the annual cost of the State Pension would increase by c. £8bn - four times higher than the current model predicts. To keep the cost of the State Pension at a similar proportion of GDP would then require a massive increase in the State Pension Age, potentially up to the dizzying heights of age 80."

Graph from OBR's "Fiscal risks and sustainability" report

|