|

|

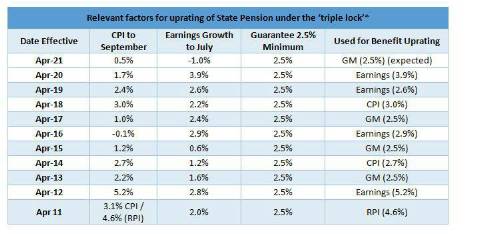

Under current rules, the State Pension is increased by the ‘triple lock’ which is the highest of earnings growth, price inflation or a 2.5% minimum guarantee. The price inflation figure used is the CPI annual rate for the year to September, which was announced today as 0.5%. The earnings growth figure used is that to July, (seasonally adjusted and including bonuses) which was already announced as minus 1%. This means the 2.5% guaranteed increase will kick in, offering pensioners 2% above inflation. |

Steven Cameron, Pensions Director at Aegon comments: “Pensioners are set for another inflation-busting increase to their state pension next April, making it three years in a row, as the September price inflation measure was confirmed as just 0.5%. This is one of the three measures setting the 'triple lock’, along with earnings growth to July which was minus 1% and a 2.5% minimum guarantee. This means subject to any last-minute changes and final Government confirmation, pensioners should receive a 2.5% increase to their state pension meaning someone on the full new state pension of £175.20 per week will receive an increase to £179.60 or an extra £4.40 per week. “Since April 2019, the state pension has received an above inflation increase with the 3.9% increase in April 2020 2.2% higher than price inflation and next year’s exceeding inflation by a further 2%. While this will be welcomed news in a difficult climate for pensioners, concerns remain over both the affordability and intergenerational fairness of maintaining the triple lock. “The state pension is not funded in advance but on a ‘pay as you go’ basis from today’s workers’ National Insurance contributions. The Chancellor will no doubt be facing difficult decisions over whether he can afford to retain the triple lock as he supports the economy through wave two of the pandemic and looks ahead to getting the nation’s finances back on track.”

|

|

|

|

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd