“With many people’s saving facilitated via their employer, the self-employed have long been a concern when it comes to pension savings. Retirement Annuity Contracts were introduced as far back as 1956 for this group, paving the way for the personal pensions we have today. However, the latest findings show the situation has worsened dramatically, and this is now a ticking time bomb for the UK self-employed workforce.

“Not only has the composition of the self-employed changed since the first Pensions Commission, but so too have their levels of pension participation. The proportion saving into a pension in a typical month has fallen sharply from around 50% in the late 1990s to less than 20% today, dropping even further among those who rely solely on self-employment income.

“The long-held assumption was that the self-employed would build wealth for later life through other means, such as property ownership. However, the nature of self-employment has changed significantly. The rise of the gig economy means the self-employed population is larger, with lower and more variable earnings than employees. Women are also making up a growing share of this group and, while self-employment offers flexibility, it risks further widening the gender pensions gap.

“This makes pension saving even more important and valuable.

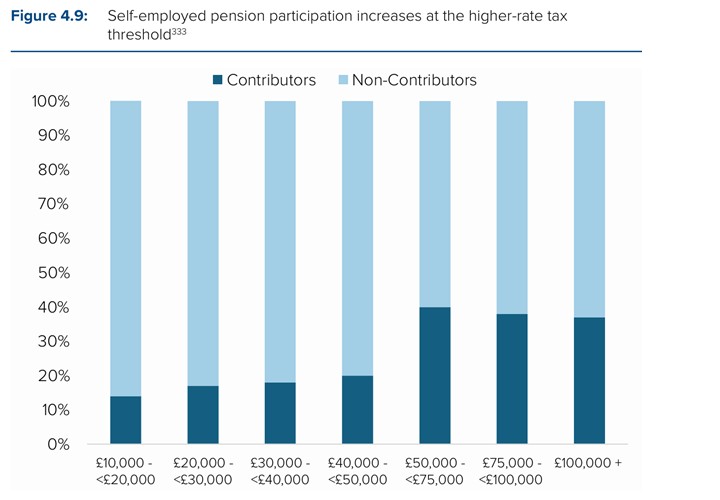

“Yet for many, pensions for the self-employed remain a well-kept secret. Outside of more affluent groups, engagement is low and even among higher earners uptake remains limited, despite significant tax advantages.

“The challenge is partly about education and accessibility. If more people understood that a £10,000 contribution could be boosted to £12,500 or even £16,667 through tax relief, and may help retain income assessed benefits such as child benefit, it could become a much more attractive option.

“Pensions are also still seen as complex. Knowing where to start, how to invest, and which product to choose can be significant barriers. While SIPPs are common among the self-employed, they tend to appeal to more financially confident individuals. Expanding access to simpler, workplace-style solutions and improving awareness through digital tools and industry collaboration could help drive engagement.

“Young self-employed people are particularly at risk, with only around one in 40 under age 45 saving for the future. It would be wrong to assume this group lacks financial awareness, many are or will be running their own businesses. The issue is more about understanding the scale of the challenge and the options available to them.”

|