|

|

Savers are being urged to ‘stop and think’ before accessing their retirement pot during ‘peak withdrawals season’ in April, May and June |

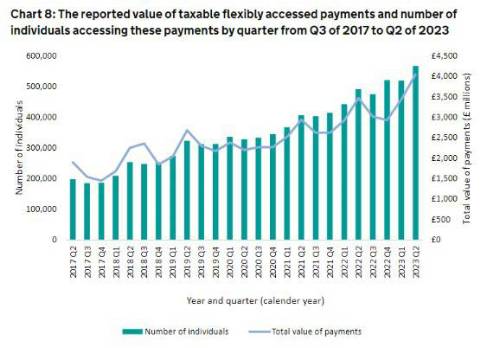

Flexible pension withdrawals traditionally spike at the start of the tax year, as savers take advantage of a fresh set of tax allowances The only exception to this was in 2020, when uncertainty caused by the pandemic saw savers pause or reduce withdrawals With Brits facing higher living costs as a result of persistently high inflation over the last two years, withdrawals could hit new highs in April, May and June 2024 Sustainability of withdrawals, investment growth and pension tax allowances among key considerations for those considering dipping into their retirement fund Tom Selby, director of public policy at AJ Bell, comments: “The start of the tax year is traditionally peak pension withdrawal season for people with defined contribution (DC) pensions, with hundreds of thousands of savers dipping into their retirement pot – many for the very first time – in order to take advantage of a fresh set of income tax allowances. This can be a perfectly sensible thing to do provided you have a well-thought-through withdrawal plan. “This time last year saw a sharp spike in withdrawals, with a record £4 billion of taxable payments taken from pensions flexibly by 567,000 people during the quarter, at an average of £7,100 per withdrawal. This represented a 17% increase in the value of withdrawals compared to the same quarter in 2022, with surging inflation undoubtedly a significant factor as many savers were forced to turn to their pension pots to make ends meet. “While inflation is now cooling, the pain of two years of rising prices is still being felt by households, with millions braced for significant spikes in costs as they prepare to remortgage in a world of much higher interest rates. Given these ongoing pressures on Brits’ finances, we are likely to see another surge in pensions access over the next three months. “Anyone considering accessing their pension for the first time or hiking withdrawals to cope with rising living costs should stop and think before making a rash decision. Taking money out of your retirement pot early or withdrawing too much, too soon could have disastrous consequences over the long term. “What’s more, pensions benefit from generous tax treatment on death, meaning it often makes sense for your retirement to be the last asset you touch.”

Source: HMRC (Private pension statistics commentary: September 2023 - GOV.UK (www.gov.uk)) Five reasons to ‘stop and think’ before accessing your pension pot early or hiking withdrawals

1. Early access increases the risk of running out of money in retirement

Pensions can be accessed from age 55, with this minimum access age due to rise to 57 in 2028. For most people, however, the aim of the game remains providing an income to support your lifestyle throughout retirement. Withdrawing too much, too soon from your fund means you’ll increase the risk of running out of money early – and potentially being left relying on the state pension.

Take a healthy 55-year-old with a £100,000 pension pot. If they withdraw £5,000 a year, increasing annually in line with inflation at 2%, and enjoy 4% annual investment growth after charges, their fund could run out by age 80. Given average life expectancy for a healthy 55-year-old is in the mid-80s – with a decent chance of living well into your 90s – such an approach would clearly create a serious risk of draining your pot early.

Put simply, if you raid your pension pot early, you’ll either need to keep your withdrawals very low, potentially harming your quality of life later in retirement; find other sources of income; or face up to the prospect of your pot running out sooner than planned and being left relying solely on the state pension.

2. Early access could also see you miss out on investment growth

The sustainability problems created by taking an income early from your pension will be compounded if you miss out on investment growth at the same time. While savers have total freedom over how to invest their retirement fund, it usually makes sense to take a bit less risk when you start drawing an income from your pot.

At the very least you will need to sell some of your investments to make a withdrawal, meaning you might have somewhere between 12-24 months of income held in cash. This lower risk portfolio will inevitably have lower return expectations over the long term.

What’s more, anyone taking money out of their pot early will have any investment growth applied to a smaller pot of money.

For example, take someone with a £100,000 pension pot. If they withdraw £10,000 on their 55th birthday and enjoy 4% investment growth after charges, by age 65 their fund could be worth £133,000. If they didn’t take the £10,000 out and enjoyed the same level of investment growth, by age 65 their fund could be worth £148,000 – £15,000 more.

3. You could trigger a big cut in your annual allowance

Anyone considering withdrawing taxable income from their retirement pot for the first time needs to be aware of the severe impact it will have on their ability to save tax efficiently in a pension in the future.

Taking even £1 of taxable income from your pension flexibly will trigger the money purchase annual allowance (MPAA), potentially significantly reducing the amount you can save in a pension tax efficiently. Chancellor Jeremy Hunt at least reduced this cliff edge by increasing the MPAA from £4,000 to £10,000, but that is still a lot less than the £60,000 annual allowance.

Furthermore, if you trigger the MPAA you will lose the ability to ‘carry forward’ unused pensions allowances from up to three previous tax years.

If you are struggling to make ends meet and your pension is the only asset available to support you, consider just taking your tax-free cash (or a portion of your tax-free cash) as this won’t trigger the MPAA.

Alternatively, it is also possible to access up to three personal pensions worth £10,000 or less – and unlimited occupational pensions – without triggering the MPAA, provided you exhaust the entire pot in one go.

4. Hiking withdrawals risks hurting sustainability

It is not just those accessing their pension early who could be at risk during this cost-of-living crisis – a period of high inflation presents a major challenge to anyone drawing a retirement income.

Most people will want their pension withdrawals to increase in line with inflation in order to maintain their living standards. However, if inflation continues to run above the 2% Bank of England target, this will have a big impact on the sustainability of a withdrawal plan.

Consider a healthy 66-year-old with a £100,000 fund who wants to withdraw £5,000 a year from their pension, rising in line with inflation.

If inflation is 2% a year throughout their retirement their fund could last until age 91. If inflation is 4% a year, however, then the fund could run out by age 85 – a full six years earlier.

Inflation is unfortunately entirely out of our control. However, anyone planning to increase their withdrawals to maintain their spending power should think about the impact on the sustainability of their plan.

It’s also worth taking a step back and thinking about your own personal inflation rate. The figures produced by the ONS are an average based on a weighted basket of goods, but your own inflation may be higher or lower depending on what you spend your money on.

Sit down, tot up your costs and income sources, and try to design a sustainable retirement income strategy that meets your needs.

5. Don’t forget about inheritance tax

Pensions are no longer just about providing an income in retirement. Rules introduced alongside the pension freedoms mean savers can pass on leftover pensions completely tax free if they die before age 75. Where the pension holder dies after age 75, the remaining funds will be taxed at their recipient’s marginal rate when they make a withdrawal.

For those who want to leave assets to loved ones, it therefore often makes sense to leave as much of your pension untouched as possible in order to minimise your tax bill.

This means when you come to flexibly access your pension for the first time, you should think not just of your retirement income strategy but also your IHT plans. If you have money held in an ISA, for example, this will count towards your estate on death.

For those who want to pass their pension on to loved ones, it’s also important to ensure your nominated beneficiaries are up to date so the right people inherit your pot.

|

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd