|

|

With debate on-going around whether the LISA will prove popular or lead to the death of pensions, Richard Parkin Head of Pensions at Fidelity International has crunched some numbers and argues that while time will tell on popularity, the economic case for saving in a LISA - as it will inevitably be called - is pretty strong. |

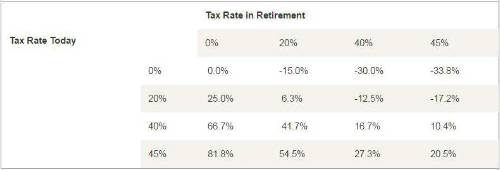

“Suggestions that the LISA will undermine pension savings are, we think, overdone. The idea that people will opt out of pensions to save for house purchase in a LISA seem to confuse cause and effect.Those who are determined to buy their own home but can’t afford to do that and contribute to their workplace pension will surely opt out of the pension in any case. The LISA just gives them a product that they can do that in more tax effectively allowing them to get back into retirement saving sooner. “Beyond this, it will clearly remain best advice for people to stay in their workplace pension and get any employer contribution available to them. But saving in a pension beyond this level may be questionable. Generally anybody paying basic rate tax today will be better off making additional saving in a Lifetime ISA rather than saving in a pension. The government subsidy to the LISA gives savers a 25% uplift whereas pensions will provide only a 6% uplift for those still paying basic rate tax in retirement and those who become higher rate payers actually lose 12.5%. “The situation for those paying higher rate tax is more complex. Those who expect to be basic rate payers in retirement should stick with the pension as this will give them a 42% uplift on their original saving whereas those who will remain higher rate payers will be slightly better off (7%) in the LISA. “It has to be remembered that the LISA is only available to those under 40 and is limited to £4,000 of savings a year. Older savers with more to invest will still find pensions the best option. “Overall then we see the Lifetime ISA as a valuable addition to the savings landscape. It will make a meaningful difference for younger savers who value flexibility and for whom the current system of pension tax-relief offers little.” Table: Comparing Pension and Lifetime ISA – Uplift from Saving from Taxed Income into a Pension

|

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd