|

|

Artificial Intelligence (AI) adoption accelerates across the insurance ecosystem, yet underlying market realities temper widespread optimism. While intense competitive pressure forces insurers, brokers and reinsurers to fast-track AI-enabled tools, critical systemic risk concerns persist. Industry stakeholders increasingly flag structural vulnerabilities, warning that current models lack the requisite maturity for enterprise-wide deployment, reveals GlobalData. |

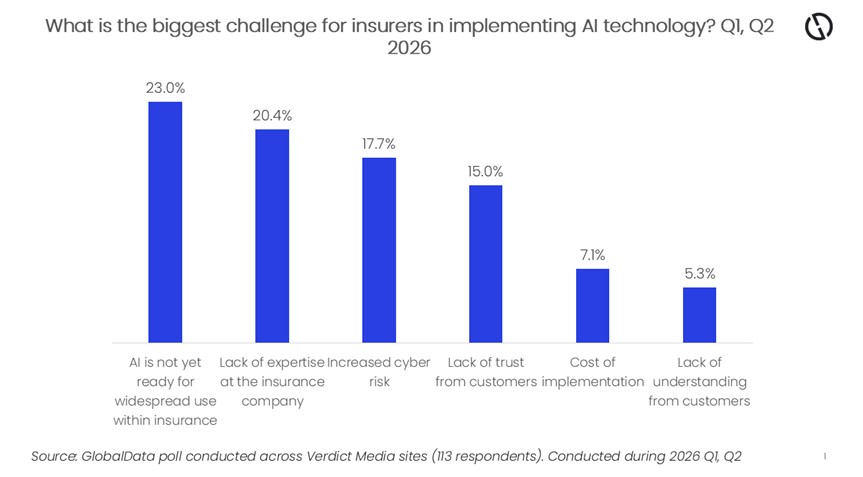

A poll conducted by GlobalData in Q1 and Q2 2026 (113 respondents) found that AI itself was not ready for widespread use within insurance, with nearly a quarter of respondents selecting it.

Ben Carey-Evans, Senior Insurance Analyst at GlobalData, explains: “This might be because use cases to date are largely around customer service and chatbots, rather than full-scale implementation. Regulation has not fully caught up yet and there is concern around who is liable for mistakes made by AI.” A lack of expertise at the company level was the second-highest concern. Interestingly, the poll revealed a higher level of concern that insurers were ready for it than consumers were. Only 5.3% of respondents felt lack of understanding from consumers was the greatest challenge. Carey-Evans adds: “This is likely because consumers are seeing increased usage of AI across all industries and companies they interact with and are becoming accustomed to it.” GlobalData’s Job Analytics shows that there were 63,293 active jobs related to AI expertise in insurance in 2025. This is the highest year ever and a 50.9% increase on 2024. This highlights that insurers are trying to address the lack of expertise gap via employment, but AI is growing so quickly it is hard to keep up. Carey-Evans conlcudes: “There will always be challenges to implement a technology with such high expectations as AI across the value chain. Insurers need to ensure they have the right expertise in place and fully understand the technology. Targeting certain areas at a time, such as customer service, customer acquisition or claims could help make the scale manageable.” |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd