|

|

With improved scheme funding levels and regulatory change to allow more flexibility in releasing surplus within defined benefit (DB) schemes expected, the prospect of running-on your DB scheme continues to be a hot topic in the pensions industry. The recent government response to consultation on options for DB schemes lays the groundwork for trustees and sponsors to work together to generate and release surplus in future. In this article, we share how DB schemes can tailor their investment strategy to support surplus generation and capitalise in a run-on period. |

By Chris Pritchard, Principal and Co-Head of Insurance Investment at Barnett Waddingham Many schemes have de-risked to the point of holding portfolios invested entirely in investment-grade corporate bonds and hedging assets with the expectation of transacting a buy-in. With run-on now a very credible alternative, a lot of these schemes will be in a position where they have de-risked too far. To quote Charles Darwin: "It is not the strongest of the species that survives, nor the most intelligent, but the one most responsive to change." Trustees should consider a change to their investment strategy as both the regulatory regime and macroeconomic landscape shift.

By (re-)introducing other income producing asset classes you can:

Increase expected return while also increasing the probability of paying member benefits over the period of run-on as a surplus buffer builds up.

Better diversify the portfolio by reducing the exposure to a single return source, increasing certainty of paying benefits and generating a surplus. Increase the amount of surplus that can be extracted.

Our approach focuses on diversifying sources of return within income producing assets to give pension schemes a more efficient investment strategy, allowing them to run on for longer and extract more surplus without putting the security of member benefits at risk.

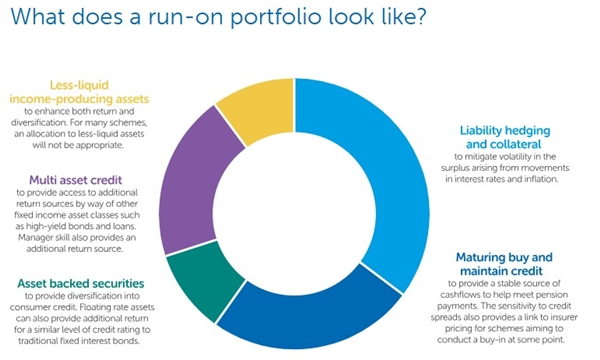

Four key principles for a run-on strategy To achieve this, there are four key principles that any run-on strategy should adopt: 1. Return generation A well-constructed allocation to assets that generate a return above cash should form a part of the strategy in order to build a surplus. Schemes with longer run-on periods are more likely to be in a position to capture longer-term investment opportunities, such as those associated with megatrends, creating additional value over time. 2. Risk control The security of member benefits is paramount. Key investment risks should be managed, such that there remains a very high degree of confidence in member benefits being paid with minimal reliance on employer support. The period of time that a scheme runs-on for will impact the degree (and types) of risks it is exposed to. For example, those with longer time horizons may be more highly exposed to physical climate risks. 3. Buy-in aligned Most schemes that run-on will do so for a period of time, before eventually securing a full buy-in of the liabilities. The investment strategy should therefore be consistent with this goal, including maintaining sufficient liquidity to allow the scheme flexibility to pivot towards a buy-in at short notice if circumstances should change. 4. Liquidity The portfolio should have a high allocation to liquid assets, so that the scheme can pivot to a buy-in should the sponsor covenant deteriorate, or should a change in attitude from either trustees or sponsor result in a shortening of the run-on timeframe. This may mean limiting the use of illiquid funds, though a modest allocation can still offer a valuable source of returns and income generation if the timescales for investing align well with the expected time running on. A well-diversified income producing portfolio can achieve all of these objectives.

Less-liquid income-producing assets can include true diversifiers such as insurance-linked securities. There has also been significant recent developments in the industry in evergreen structures for illiquid assets – giving schemes access to assets such as private credit and infrastructure with greater liquidity and flexibility than investing in closed-ended funds. Allocations should not be static – it is important to be dynamic across different asset classes to maximise value as the scheme’s funding position changes, and as market conditions change. We will be publishing stand-alone blogs on our thoughts on the best approach to investing in each of these asset classes in due course.

What about other asset classes such as equities?

Greater security and certainty of return.

Providing additional benefits to members (either in the form of additional DB or DC benefits). Again, for this purpose, we favour income producing assets as these types of assets move in a similar way to liabilities provide a greater degree of certainty to the security of additional benefits.

What should trustees be doing?

As mentioned at the start of this article, for schemes invested entirely in gilts and corporate bonds, reintroducing other income producing asset classes will allow you to:

Increase expected return while also increasing the probability of paying member benefits over the period of run-on as a surplus buffer builds up.

Better diversify the portfolio by reducing the exposure to a single return source, increasing certainty of paying benefits and generating a surplus. Increase the amount of surplus that can be extracted. Switching a 50:50 credit and gilts portfolio to an investment strategy that is aligned with our portfolio above could generate an additional return of £50m+ for a £500m pension scheme running-on for 10 years. |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd