|

|

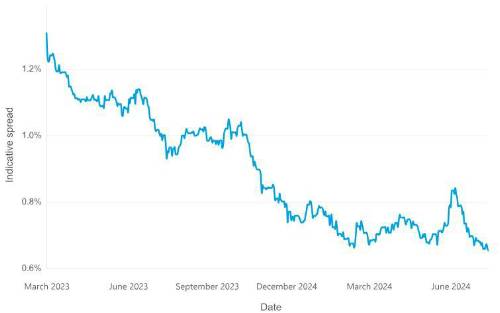

Despite a slight increase in recent weeks, credit spreads are low – as low as they have been for a very long time. Following spikes during the Covid-19 pandemic and again over 2022, when AA-rated bonds (a rating often taken to represent a high-quality issuer of bonds) could provide returns well in excess of 1% above gilts each year, we now find ourselves in a world where you need to go below A-rated bonds if you want a return of gilts + 1% p.a. |

By Paul Houghton, Partner at Barnett Waddingham

What are credit spreads?

When we talk credit spreads, we mean the size of the yield available on corporate bonds above that on a Government bond – theory says the yield, or spread, exists to compensate for the greater risk from holding a bond issued by a corporate compared to one issued by the Government, and the riskier the company issuing the bond, the higher the spread.

Impact of low credit spreads on pension schemes

Discussing why credit spreads are so low is an interesting debate, but not for this article. The relevant point for us here is that because credit spreads are lower, the value of the corporate bonds we’re holding is now higher. Which feels like good news for pensions schemes – higher asset values and so better funding levels.

De-risking strategies and their pitfalls

As we know, many pension schemes currently find themselves with very strong funding positions and have sensibly decided to de-risk their investment strategy – quite often by selling equities and purchasing bonds, both corporate and Government.

But is this a cycle schemes have walked into? Corporate bonds increase in value. Funding looks better. Pension scheme de-risks by selling equities and purchasing corporate bonds, at a time when we have just said they’re expensive.

Is the funding improvement real?

But more than that, is all of the recent improvement in funding level even real?

As we explore in the next section, most schemes have a fixed long-term funding target which doesn’t automatically move in line with credit spreads – should this target be adjusted, offsetting the increase in the asset value? Arguably it should be.

And so does this mean that schemes which haven’t been adjusting their funding target have been de-risking and buying corporate bonds, at a time when they’re expensive, and on the back of a misleading funding improvement?

The key message here is that investment consultants and actuaries should be talking to each other before de-risking. If an improvement in the funding position is driven by corporate bond yields and your asset strategy is to hold corporate bonds, consider whether the funding improvement is real, or just a quirk of the current market. Check before you buy more corporate bonds!

How does this fit in with the new DB Funding Code?

While we’re talking credit, credit to The Pensions Regulator (TPR). The new DB Funding Code – which was laid in Parliament on 29 July and will come into force for all valuations with an effective date of 22 September 2024 – means that all schemes need to aim for a long-term funding target of low dependency. As was widely expected, TPR has confirmed a long-term target of 'gilts + 0.5%' can expect not to face any regulatory scrutiny.

But could the recent fall in credit spreads mean that schemes should pause before deciding that a gilts +0.5% target is appropriate?

Reevaluating long-term funding targets

Let’s think about that long-term target. A default strategy will often be to achieve full funding on a gilts + 0.5% p.a. basis, alongside a low-risk investment strategy consisting primarily of gilts and corporate bonds. Such a strategy will clearly meet the regulator’s expectations under the new funding regime.

And in a world where credit spreads on high quality corporate bonds are above 1% p.a., it all adds up – you can hold a portfolio consisting of 50% gilts and 50% high quality corporate bonds (it would be more nuanced than this in practice) and not need to worry about whether this can support your discount rate of gilts + 0.5% p.a.

Adapting to current credit spread levels

However, things don’t look quite so neat in a world where credit spreads are at the levels they are today. Suddenly our long-term funding basis doesn’t quite fit with our long-term investment strategy. So what does this mean? If the maths doesn’t stack up then we have two options: Run a bit more risk in the investment strategy to support an expected return of gilts + 0.5% p.a. The new regulations give schemes leeway as to what 'low dependency' looks like (and, strictly speaking, don’t actually require schemes to invest in a low dependency way – only that they take account of the objective to do so). But taking more risk inevitably raises the question of whether the revised investment strategy is still consistent with the regulatory expectations. Moreover, the additional risk may not sit comfortably with all trustees and sponsors. Reduce the discount rate to below gilts + 0.5% p.a. This means schemes can still invest in low-risk assets only (high-quality bonds) if desired, but it makes the long-term funding target more difficult to achieve. It is also a bit of a mindset shift for us all, as we have got used to gilts + 0.5%.

Long-term funding targets and market conditions

Regulatory flexibility and future considerations But after years of waiting, is there a risk that TPR will need to re-think the gilts +0.5% long-term target after the new Funding Code goes live? While the contents of the final Funding Code and the new regulatory approach to assessing valuations, (currently) suggest that gilts +0.5% p.a. is an appropriate target, trustees and sponsors should consider whether this indeed remains the right target for their schemes. |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd