Nearly half (43%) of UK adults aren’t confident the six-month deadline for paying inheritance tax (IHT) on unused pension funds will be long enough, according to new research from Standard Life.

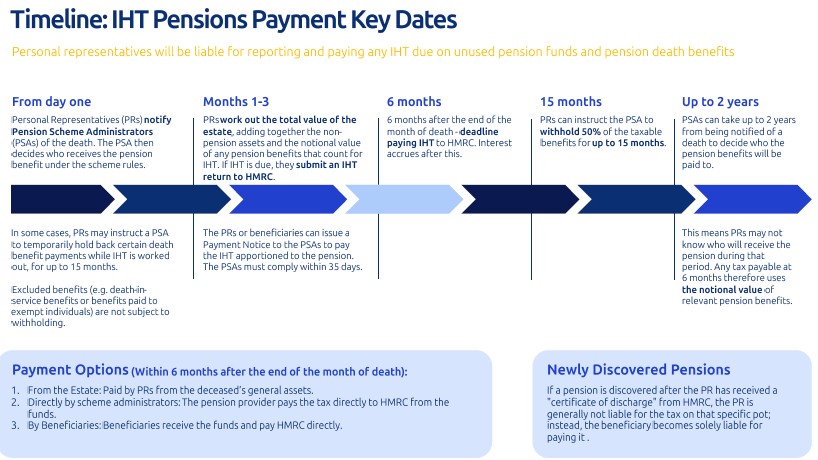

From April 2027, personal representatives responsible for administering an estate, typically family members or friends, will also need to account for any unused pension savings when determining if the estate exceeds the available IHT nil rate band. Any IHT is due within six months of the end of the month of death.

The timeline for paying pension-related IHT has attracted significant discussion, including from the House of Lords Economic Affairs Finance Bill Sub-Committee, who highlighted the practical challenges personal representatives may face in meeting this deadline.

In response, the government confirmed that the standard six-month timeline will apply from April 2027, citing the importance of consistency in the treatment of estates for IHT purposes.

Neil Jones, tax and wealth planning specialist at Standard Life comments: “With the April 2027 changes fast approaching, attention is turning to the practicalities of how IHT on pensions will be paid. The government confirmed last year that responsibility will lie with the estate’s personal representatives, usually family members or friends.

“One of the biggest challenges will be identifying all the deceased’s pension pots. Those approaching retirement today typically have two or three pensions, but younger generations are expected to have 11 or 12 pots over their working lives, largely due to job mobility and pensions auto-enrolment. Consolidating pension pots may make things simpler for personal representatives to manage depending on circumstance, but it’s important to understand whether bringing these together could mean losing any valuable features or guarantees before making changes.”

Confidence low among over 55s

The research also highlights limited confidence among older adults. Only a third (32%) of people aged 55 and over think that the family members or friends appointed as personal representatives would be able to successfully manage the payment of any IHT due on pension assets.

Given estimates suggest around one in ten estates will exceed the IHT threshold by 2030, those potentially affected will need to understand who is responsible for paying IHT on pensions, how the process works, and when payment must be made.

Standard Life sets out the Pensions IHT payment timeline and responsibilities, from April 2027:

The impact of bereavement on financial decision-making

Neil Jones, continues: “The impact of bereavement on decision-making should not be underplayed. Research shows that grief can be associated with reduced functional capacity, affecting decision-making not just emotional wellbeing.

“This can make it more difficult for personal representatives to navigate administrative tasks and meet deadlines. For families coping with loss while managing an estate, planning ahead to reduce the administrative burden is therefore important. Engaging a professional, such as a solicitor, can help ease this responsibility on family members during a challenging time.

“While the changes may feel complex, taking simple steps today, such as keeping pension records up to date, can help make things much easier for loved ones in the future.”

|