In a financial journey often shaped by the ups and downs of life, decisions made now can have a lasting impact. With the end of the tax year approaching, directing a £5,000 annual bonus into a pension for just four years could add almost £40,000 to someone’s total retirement pot, according to Standard Life, a retirement specialist focused entirely on retirement savings and income.

With many people currently under-saving for retirement, even small one-off pension contributions can have a significant effect over time. While not everyone receives a bonus payment, and for those that do the amount can vary, it can present an opportunity for people to strengthen long-term savings and engage more actively with their financial future – helping them build greater financial security in later life.

It’s no sacrifice? Why bonus sacrifice can make such a difference

One option available to some employees is bonus sacrifice, where part or all of a bonus is paid directly into a pension before tax and National Insurance (NI) are applied. While it won’t be right for everyone, understanding how it works could help people make more of their money and think more confidently about retirement planning. It’s worth being aware that the government has announced plans to limit the NI exemption for salary pension contributions to £2,000 a year from 2029, but there are no changes for now.

Many workers may not realise how sharply deductions can reduce a cash bonus. Once income tax, National Insurance (NI) and - for many - student loan repayments are taken, a £5,000 bonus can shrink to as little as £3,150 in take-home pay for a basic rate taxpayer. If the same £5,000 is paid directly into a pension through salary sacrifice, however, the full amount is invested before these deductions.

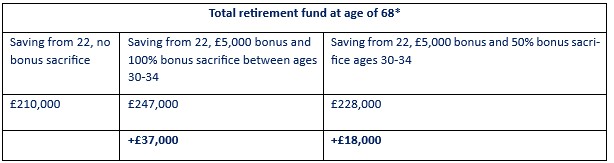

Over time, that difference in how a bonus is treated can have a significant impact on retirement outcomes. New Standard Life analysis shows that someone who starts work at age 22 on a salary of £25,000 and pays the minimum monthly auto-enrolment contributions (5% employee, 3% employer) could build a retirement pot of around £210,000 by age 68, allowing for inflation and charges. Someone who receives a £5,000 bonus at age 30 and diverts it into their pension for four consecutive years could increase their pot to £247,000 in today’s prices - £37,000 more.

*assuming 3.50% salary growth per year, and 5% a year investment growth. Figures allow for 2% inflation. Annual Management Charge of 0.75% assumed. The figures are an illustration and are not guaranteed. Earning limits not applied. The value of investments can go down as well as up and may be worth less than originally invested. Assuming bonus sacrifice contributions are paid before 6 April 2029.

Clearly, there’s a balance to strike between enjoying today and preparing for tomorrow - and bonus sacrifice doesn’t have to be all or nothing. Someone in the same scenario who chose to keep half of their bonus for now and direct the other half (£2,500) into their pension for the four years, could see an £18,000 boost, with a pot of £228,000 by the age of 68.

Some employees could see an even bigger uplift if their employer passes on some or all of the employer NI savings generated through salary sacrifice.

Mike Ambery, Retirement Savings Director at Standard Life plc said: “Salary sacrifice has long been one of the simplest and most effective ways for people to boost their pension, yet many still overlook how powerful it can be - particularly when it comes to bonuses.

“It’s always going to be tempting to earmark any bonus you receive for the demands of everyday life – whether that’s paying for a holiday, buying a new car, or making home improvements. And in today’s high-cost world, many people may simply need the money for day-to-day essentials, from living costs to paying off debts. However, after deductions are taken into account, cash bonus payslips can look incredibly disappointing. Diverting some or all of that bonus into a pension can help people make more of their money, engage more confidently with their financial future, and ultimately achieve better outcomes and greater financial security in later life.

“What really matters is recognising that progress doesn’t have to come from big or perfect decisions. You don’t need a large bonus to start making a difference - even relatively small, one-off pension contributions can add up over time. For many people, understanding that every contribution counts can help build confidence on their journey to and through retirement.”

Mike answers key bonus sacrifice questions

1. What is bonus sacrifice and why does it matter?

“Bonus sacrifice is when you choose to give up some or all of your bonus and have it paid directly into your pension instead. Because the money goes in before tax and National Insurance, you usually pay less in deductions and more of what you’ve earned ends up working for your future. Over time, that head start can make a real difference, as the money has longer to grow and can significantly boost your pension by the time you retire.

2. Do I have to sacrifice my whole bonus?

“No, you can usually choose how much of your bonus to sacrifice. Even sacrificing part of a bonus – or doing it for just a few years – can meaningfully increase your retirement savings, while still leaving you with money to enjoy today.

3. What should I check before deciding?

“It’s worth confirming whether your employer offers bonus sacrifice and how it affects things like take-home pay and other benefits. It’s also important to think about whether you might need that bonus for short-term expenses, as pension money is locked away until later life – the minimum age to access private pensions is set to rise to 57 on 6 April 2028.”

|