|

|

Our 2026 survey results provide a detailed view of how all 11 active insurers are progressing schemes from initial buy-in to full buyout – the point at which legal responsibility for providing members’ benefits transfers to the insurer. It has been a record year for buyouts and momentum is expected to continue into 2026. Our findings, based on insurer data up to 31 December 2025, show how quickly schemes are moving through the process, where delays most commonly arise, and how market capacity is evolving in response. |

By Beth Allison, Principal and Head of Post-Transaction and Wind-up, Barnett Waddingham Buyouts at record levels

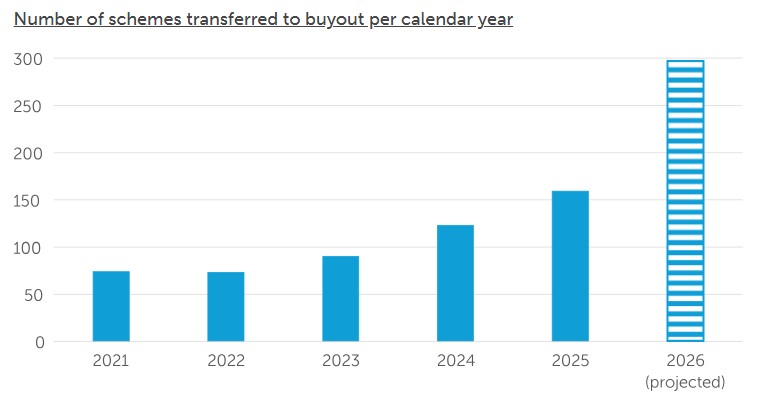

2025 marks another milestone year, with almost 160 schemes completing buyout – a 30% increase on 2024. Insurers anticipate this upward trajectory will accelerate, with the number of buyouts projected to almost double in 2026, when around 300 schemes are expected to reach buyout.

Source: Barnett Waddingham 2026 Insurer survey This is perhaps not surprising given the sharp increase in the number of schemes transacting with insurers over recent years. However, it brings sharper focus to a key question: how quickly are schemes progressing from buy-in to buyout, and how does that compare with the number of new buy-ins being written? The post-transaction bottleneck – are things improving?

Despite the growing volume of buy-ins, the journey to buyout remains lengthy for many schemes:

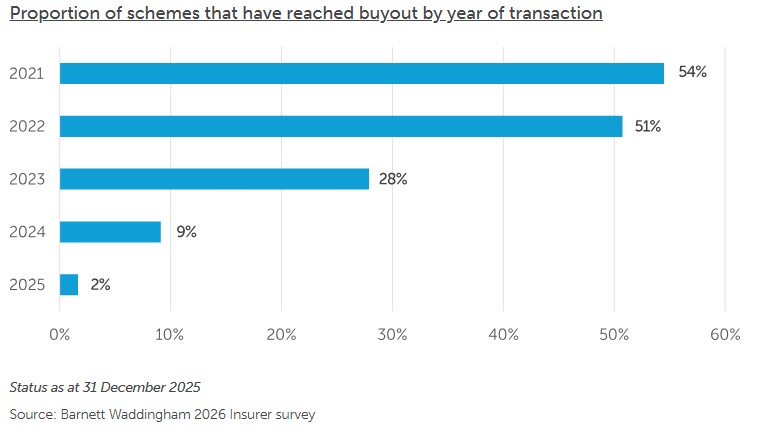

Just over half of buy-in transactions from 2021 have now reached buyout, highlighting that almost half of schemes in this cohort have spent at least four years on the path to buyout without yet reaching this milestone.

Half of 2022 transactions have progressed to buyout, reaching this milestone within three years.

Only 28% of 2023 transactions have so far completed buyout, falling sharply to 9% for 2024 and just 2% for 2025.

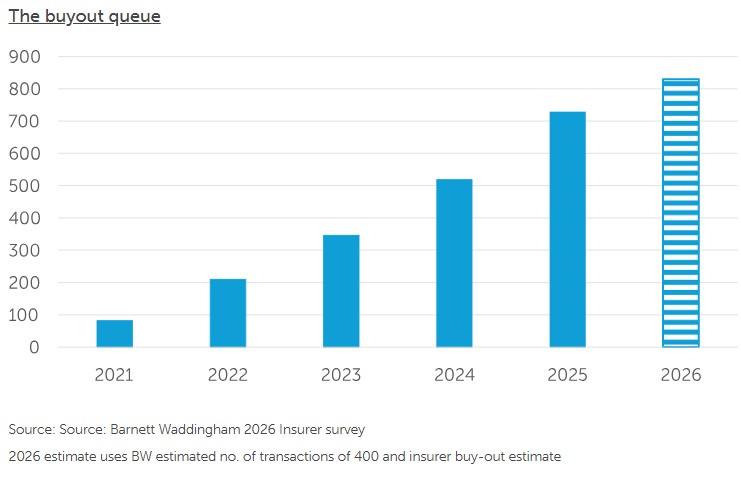

This highlights the ongoing challenge: while buy-ins are becoming increasingly common, the final steps to buyout and wind-up still require substantial time and preparation. Three years to buyout is becoming accepted as the current industry norm, as reflected by The Pensions Regulator in its recent modelling on the evolution of DB schemes. There are, however, some encouraging signs. Almost a fifth of transactions written in 2023 and 2024 have already moved through to buyout, demonstrating that schemes can progress quickly, within one to two years, when they are well prepared and advanced with their data and benefits work. This aligns with the patterns we are seeing across our own cases, where a quarter of our schemes in this 2023-2024 cohort have reached buyout. Looking at older transactions, our focus on preparedness means all of the schemes BW advised that transacted in 2021 have already bought out, compared with only 54% across the wider market. The buyout pipeline is set to keep growing in 2026. While insurers project an increase in buyout capacity, Barnett Waddingham’s estimates suggest buy-in activity will surpass 400 transactions this year. This means that 2026 is likely to be another year with more buy-ins than buy-outs, adding further volume to the pipeline of schemes progressing toward full buy-out and eventual wind-up. As a result, the buy-out queue is projected to grow to more than 800 schemes.

It is worth noting that some schemes reflected in this buyout queue will have will have chosen to remain in a long-term buy-in and so will not place demands on insurers’ onboarding and administration capacity. However, most schemes are still expected to move directly to buyout in time. This makes it more important than ever for schemes to be well-progressed with data and benefit work in order to move smoothly through the post-transaction process and secure insurer capacity. What’s behind the delays?

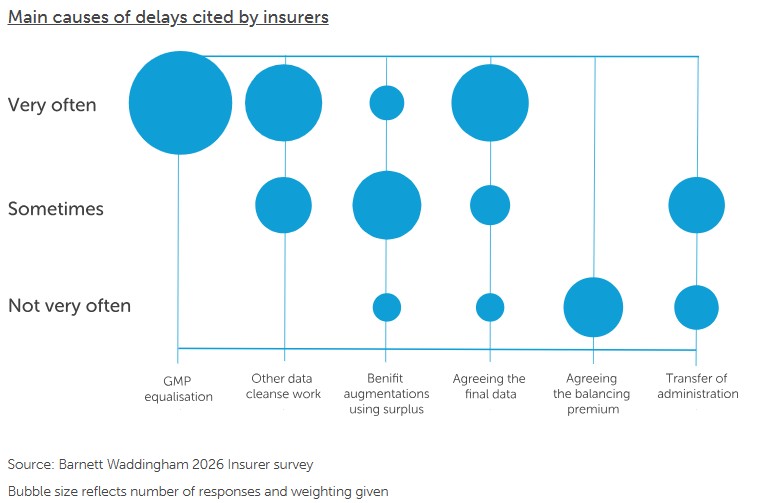

Insurer respondents continue to report a consistent set of challenges that slow progress to buyout:

GMP equalisation stands out as the most frequently cited cause of delay.

Final data agreement and broader data-cleansing requirements also feature prominently.

Less common, but still significant, issues include unexpected consultation periods and last-minute changes after final data has been agreed.

Encouragingly, many of these blockers are expected to reduce over time. As more schemes address data quality, benefit rectification and GMP equalisation before entering the market, the post-transaction journey should become smoother and more predictable. This supports our view that the most significant delays usually arise from scheme-side tasks rather than insurer capacity. Market composition: newer entrants gain ground

The buyout market remains dominated by the largest insurers, but the shape of the market is beginning to shift. Over the past five years, the top three insurers – Aviva, Just and L&G – have delivered 80% of all buyouts. Looking ahead to 2026, the top three’s share is projected to fall to around 60%.

This shift is driven by:

Increased competition and appetite in recent years, widening the spread of buy-in transactions across insurers.

Growing capacity from established insurers as they expand post-transaction teams and streamline processes to clear backlogs.

Significant growth potential for newer entrants, many of whom expect buyout figures to scale faster than those of the established insurers.

As a result, schemes can expect a broader range of solutions and more capacity across the market in the years ahead. Looking to 2026: a market investing for speed and scale

To support rising transaction volumes, insurers are continuing to invest heavily in post-transaction resources. The average team size now stands at around 50, with further increases planned to help schemes move efficiently to buyout.

Insurers are also introducing innovative ways to streamline the post-transaction journey, including insurer-led data-cleansing support, more standardised and simplified processes, and solutions such as direct insurer GMP equalisation implementation to shorten timescales. Together, these developments point to a market focused not only on increasing buyout capacity, but also on improving the overall experience and reducing friction for schemes preparing for buyout and wind-up. Top tips for a successful buyout and wind-up

For schemes preparing for buyout, the most successful outcomes continue to be driven by strong preparation and project discipline. Key actions include:

Prioritising early data and benefit readiness – accelerating data-related work through advance planning and dedicated resource can prevent many of the delays insurers most frequently highlight.

Understanding each insurer’s requirements at the outset – each insurer has different processes, and having clarity on these requirements allows them to be reflected in project planning and helps avoid unexpected rework.

Completing all scheme-side actions promptly – to keep momentum and protect your position in the insurer’s pipeline.

Appointing a dedicated project manager – to maintain clear coordination across advisers and stakeholders, keep the process on track and ensure issues are managed proactively.

Beth AllisonHead of Post-Transition and Wind-up, BW: "Our survey highlights that while well-prepared schemes can reach buyout in under two years, it is becoming increasingly common for schemes to take three to four years from buy-in to buyout. This experience is likely to persist for the foreseeable future, as reflected in the projected growth of the buyout queue over 2026. Although insurer capacity continues to expand and more schemes are addressing major data challenges such as GMP equalisation before transacting, these changes will take time to work through the pipeline. They may also be offset by an increasing number of smaller schemes that are expected to buy-in over the coming years, each requiring a similar level of fixed resource. One thing remains clear: schemes that progress fastest are those that are well-prepared, with a robust data and benefit cleansing plan and disciplined project management. In a market where competition for capacity is intensifying, expert support is critical to maintaining momentum and achieving a smooth and timely path to buyout and wind-up." Post-Transaction Consultant Henna Ruparelia contributed to this article. |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd