GlobalData’s Asia-Pacific Reinsurers Database reveals that APAC reinsurers accounted for 14.2% of global reinsurance premiums in 2024, down from 15% in 2023. Overall, however, they registered a compound annual growth rate (CAGR) of approximately 1.4% during 2020–24.

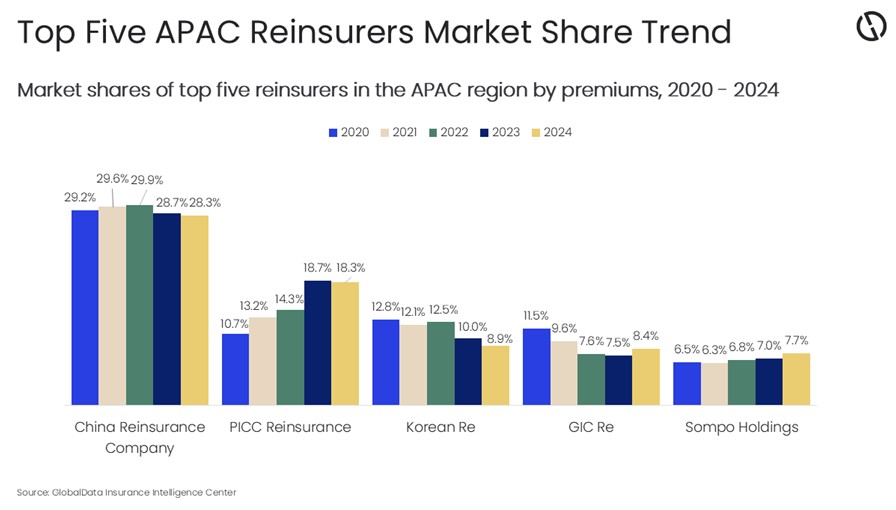

Manogna Vangari, Insurance Analyst at GlobalData, comments: “The APAC market remains highly concentrated. Indeed, its five largest reinsurers captured 71.7% of total premiums in 2024. Among them, China Reinsurance Company continued as market leader, albeit with a slight decline: its share fell from 28.7% in 2023 to 28.3% in 2024. Meanwhile, other top entities experienced modest shifts: PICC Reinsurance’s share decreased by about 0.4 percentage points (pp); Korean Reinsurance (Korean Re) declined by around 1.1pp; whereas the General Insurance Corporation of India (GIC Re) and Sompo Holdings gained approximately 0.9pp and 0.7pp, respectively.”

Looking beyond the top five, four of the top 10 reinsurance groups are based in Japan (namely Sompo Holdings, MS&AD Insurance Group, Tokio Marine & Nichido Fire Insurance, and Toa Reinsurance). The remaining six include two from China (including Hong Kong (China SAR)), one from India, and one from South Korea. Notably, among these leading groups, MS&AD Insurance Group posted the strongest premium growth during the 2020–2024 period, at a CAGR of 22.6%, followed by PICC Reinsurance at 16%.

Vangari adds: “Regarding geographic business mix, most of the reinsurance companies are heavily dependent on their global operations. However, China Reinsurance Company derives 83.5% of its business from the APAC region, while the remainder comes from its international operations, which include its CNIP and Chaucer businesses. In contrast, Korean Re holds only 25.8% of its business from APAC, while 74.2% comes from global markets.”

Turning to recent challenges, several catastrophic events have placed stress on property and casualty portfolios in the APAC reinsurance market. For example, in March 2025, a magnitude-7.7 earthquake struck Myanmar, and severe flooding affected China, India, and several ASEAN nations. In addition, Hong Kong (China SAR) suffered a fatal apartment building fire in November 2025. Similarly, Typhoon Wutip and flooding in Beijing later in 2025 further underscored persistent protection gaps and exposed accumulation risks, thereby raising questions about pricing adequacy. Alongside those natural catastrophe losses, the mid-2025 Air India Flight AI-171 Boeing-787-8 crash triggered about $475 million in claims, according to GIC Re, intensifying reinsurance pricing and aviation risk scrutiny.

In response to mounting losses, reinsurers are increasingly offering parametric reinsurance and catastrophe bonds (insurance-linked securities) to help both governments and insurers manage risk, particularly where traditional indemnity cover has gaps.

Vangari continues: “APAC reinsurers are also increasingly leveraging AI models that synthesize real-time environmental, geographic, and exposure data. These models support catastrophe modelling and risk scoring by integrating inputs such as up-to-date satellite imagery and geospatial mapping, which help reinsurers access risk across property, marine, and energy lines. This enhances loss prediction and supports treaty placements that more accurately reflect localized exposure.”

AI agents automate labor-intensive tasks—such as treaty pricing, bordereaux reconciliation, submission parsing, and clause extraction—lowering error rates and accelerating processes so specialists can concentrate on judgment-intensive work.

Major reinsurers in APAC plan to embed these tools across underwriting, claims, and policy administration by 2026, aiming for cost savings, faster decision-making, and better alignment between exposure, pricing, and reserve setting.

Vangari concludes: “Emerging trends in the region signal cautious but constructive progress for APAC reinsurers. Factors such as innovation in pricing, analytics, and automation by reinsurers is becoming essential for maintaining margin, managing risk exposure, and aligning business processes with evolving regulatory, operational, and environmental realities.”

|