By Tom Hargreaves, FIA, Associate and Senior Consultant - Corporate Actuary at Barnett Waddingham

The outcomes in these cases, summarised below, help illustrate the range of ways that schemes can influence transactions.

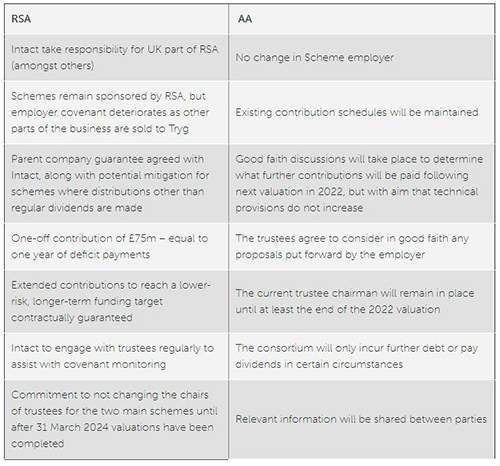

A strong starting point

The trustees of the RSA schemes have been able to use the transaction to improve the immediate security of members’ benefits through a parent company guarantee and an up-front contribution, whilst also getting a contractual guarantee for additional contributions to help meet long-term targets.

From what was presumably a reasonably strong starting point, the employer covenant was going to be negatively affected by the transaction with some parts of the business being sold elsewhere. This gave the trustees a strong negotiating position from which to agree the improvements designed to compensate for this, albeit they have recognised that they did not get everything they could have wished for.

The immediate and long-term improvements, alongside the commitment between the trustees and Intact to have an open and engaged relationship, will help move the schemes towards their endgames. The schemes are well funded, and with a longevity swap already in place covering a proportion of the liabilities it is easy to see some form of bulk annuity transaction on the horizon.

The only way forward?

On the other hand, the core pensions theme of the AA transaction is to ensure that the status quo is maintained, with a framework being agreed around the working relationship between parties going forward, rather than providing immediate improvements in security.

The AA’s financial issues around debt since being taken public in 2014 have been well publicised. However, performance in recent years has improved and has apparently been reasonably resilient to the impact of Covid-19.

In this case the transaction has a less obvious impact on the employer covenant, which gives the trustees less firm ground to stand on. Indeed, if the transaction appears to be in the employer’s best interests, then there is an argument that the best thing the trustees can do is to help facilitate it.

With this argument, you can see why agreeing to not exercise certain powers (for example around calling early valuations) can still be in members’ best interests. Perhaps the most important part of the agreement is the commitment by both parties to work together in good faith.

The outcome for the AA scheme remains uncertain. In asking the trustees to consider employer proposals in good faith, the consortium clearly have managing pension risk on the agenda and it wouldn’t be surprising to see liability management exercises being tabled with a view to bringing the scheme’s endgame forward.

We also note the explicit mention of DB superfunds in the memorandum of understanding (MoU). These vehicles expect some demand to come from schemes involved in corporate transactions and it will be interesting to see how this develops in due course.

Focus on the DB endgame

The pension schemes in each of these transactions have been treated slightly differently and one of the key reasons for this is the strength of the different trustees’ negotiating positions. However, regardless of the immediate impact, it seems likely that both cases will see schemes using the transaction as a springboard towards their endgame and reaching this sooner than previously expected.

This is not, however, a new phenomenon. The ability of the Allied Domecq Pension Fund to complete a full buy-in in 2019 was aided by a corporate transaction back in 2005 which (similarly to the RSA case) introduced a stronger financial commitment from the new owner, improved funding over time and set out a constructive approach to good governance from both trustees and sponsor. The ICI Pension Fund has also recently completed the latest in a long series of buy-in transactions since 2014, which now cover the majority of its members. ICI was acquired by Akzo Nobel in 2007, as part of which the purchaser engaged directly with the trustees to reach a satisfactory agreement before a formal offer for shares was made.

With an increasing focus within the industry on long-term objectives, we would expect this to be high up the list of trustee priorities where corporate transactions are occurring. For prospective purchasers, this highlights the importance of carrying out robust, independent pensions due diligence so that they:

Understand the journey that the scheme is on and how the transaction will affect this

Consider the options available to manage risk and potentially bring forward the scheme’s endgame

Can negotiate an outcome that meets their objectives, which may also be in the best interests of all parties

Those on the sell-side should also be thinking about this prior to going to market so that the pension information provided gives prospective purchasers with the detail they need. It may also be worth investigating whether any risk management or settlement options are viable pre-transaction, which may make the company a more attractive proposition.

|