|

|

Since the 2022 gilts crisis, there has been an increase in maturity and an acceleration in de-risking for many UK defined benefit (DB) pension schemes. Despite no two DB schemes being the same, a common feature in many de-risked portfolios are Buy and Maintain Credit (B&M) strategies. These can offer DB schemes many attributes, including exposure to credit, predictable cash flows and interest rate sensitivity, alongside other matching assets such as Liability Driven Investment (LDI) strategies. |

By Danielle Markham, Principal and Head of LDI Research and Jordan Griffiths, Associate and Senior Sustainable Investment Consultant from Barnett Waddingham Examining the long-term viability and practical implications of Buy and Maintain investment approaches for sustainability and LDI managers. Our investment research team recently undertook an in depth study into the B&M universe, considering the characteristics and credentials of B&M strategies and their managers, with a focus on sustainability. Using the conclusions of this study, this blog looks at two important considerations that DB schemes should be making, beyond the more traditional considerations of return, risk, duration, and fees. Specifically, we will consider: 1. The sustainability attributes of a DB scheme’s B&M strategy 2. Whether a scheme’s LDI manager is best placed to run its B&M strategy

Why shouldn’t maintainable be sustainable? There are many factors that may lead to an increase in the probability of default which include, but are not limited to, environmental, social and governance (ESG) risk factors. An example may be a significant environmental lawsuit that threatens an issuer’s ability to service its debt. Given those risks, we would expect all material ESG factors, alongside other wider investment risks, to be considered by investors and their B&M managers when selecting bonds to invest in and when engaging with bond issuers on key issues. The degree to which a DB scheme may go further and adopt other sustainable investment techniques, (such as specific exclusions, net zero alignment, enhanced engagements, capturing sustainable opportunities etc.), will of course depend on the scheme’s own specific sustainable beliefs and objectives. Such sustainable investment techniques can complement a scheme’s wider objectives, and we are experienced in working with our clients to help achieve this.

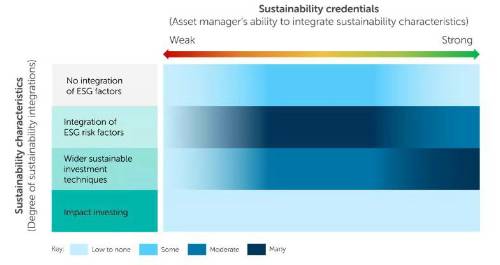

Are my sustainability goals achievable within B&M?

What about insurers and buy-out? Therefore, the largest consideration for an investor is likely to be ensuring their core objective is achieved though factors such as risk management, including management of ESG risks, would still play a role. However, this should be considered on a case-by-case basis.

However, our research shows that a strategy’s sustainability characteristics (how far the strategy goes in terms of integrating sustainability considerations) is not necessarily a reflection of the manager’s sustainability credentials (how well the manager integrates these sustainability characteristics into a strategy). Nor is it a function of the strategy’s labelling as sustainable or not – in fact, we found some vehicles without such labelling with stronger sustainability credentials than those explicitly named as ‘sustainable’.

Our study found:

Most B&M managers we reviewed have reasonable sustainability credentials – this is driven by the need to integrate sustainability characteristics well, within a competitive market. It is worth noting that within our pension scheme research we tend to consider institutional and well-resourced asset managers, resulting in a bias away from managers with weaker credentials.

Most well-resourced asset managers typically integrate ESG factors into B&M – this is driven by the recognition that such factors are financially material and should be explicitly considered. It’s integrated via their investment decision making framework and stewardship activities.

Many managers are going further on sustainability – we’re seeing lots of managers enhancing their focus on sustainability, including integrating techniques such as net zero and carbon targets, specific exclusions, enhanced engagements, and sustainable opportunities. However, there was a clear lack of strategies at the impact end of the spectrum.

The quality of the fund manager is a driving factor – strategies which aim to deliver enhanced sustainability characteristics have generally not been deemed as effective if they were offered by fund managers without a firmwide commitment to sustainable research and integration.

We should exercise caution regarding sustainability claims – our studies found the use of terms such as ‘sustainable’ or ‘ESG’ were not always an indicator of better sustainability outcomes. Strategies without such labels could have better sustainability credentials than their so-named counterparts.

Leveraging my LDI manager’s B&M expertise

Given that B&M will form part of the hedging and cashflow matching strategy for many DB schemes, we would advise asking yourself: "Is my LDI manager best placed to run my B&M strategy, or is it worth looking elsewhere?" While the answer will be scheme and manager specific, we found there were pros and cons to each approach:

Pros of holding a B&M strategy with an LDI manager Potential fee savings – several managers indicated they will consider the total fees being paid to them when deciding on discounts, so there may be opportunities to reduce fees if held together. Easier to design and build the liability hedge – although all LDI managers are able to take account of external credit holdings at a high level (which is usually sufficient), being able to manage this more accurately over time and have a shared collateral pool for segregated mandates (for example, to deal with both currency hedging of credit and inflation swap positions) may be more efficient.

Cons of holding a B&M strategy with an LDI manager Having all mandates with one manager may be a concentration risk – as schemes de-risk, it is likely the combined LDI and B&M strategies will make up a large proportion of the scheme assets. However, given neither LDI nor credit is typically actively managed, we do not consider it to be a significant concentration of manager risk to have both portfolios managed by same manager. In addition, managers have different teams managing LDI and B&M strategies which reduces this risk. The concentration of firmwide risks, such as operational, legal, corporate and/or reputational risks should still be weighed up. Transition/advisory fee – movement of assets is likely to incur fees. However, the benefits associated with the decision to move may outweigh the costs over time. This is likely to be a larger consideration for clients closer to buyout, who may have less time to deal with the initial costs of moving assets.

Next steps However, important though they are, the sustainability and operational considerations of B&M strategies raised in this blog are just two of the numerous key factors that DB schemes will need to consider as part of an investment into B&M strategies. Our recent in-depth study on the B&M universe will help us review and challenge your current or potential managers on their characteristics and credentials, both in terms of sustainability and more widely. |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd