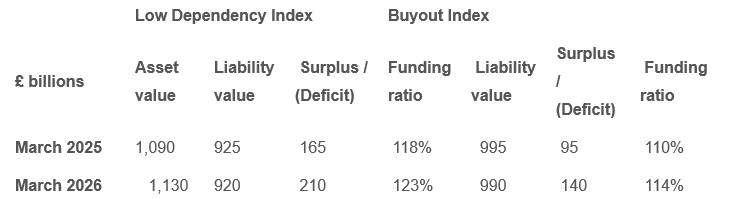

As of 31 March 2026, PwC estimates that UK DB schemes held assets totalling £1,130 billion against liabilities of £920 billion on a low dependency measure. This equates to an overall surplus of £210 billion and a funding level of 123%.

Meanwhile, PwC’s Buyout Index, which measures the estimated cost for UK defined benefit pension schemes to fully insure their liabilities via buyout with an insurer, indicated a robust funding position, with an estimated surplus of £140 billion (114% funded).

This continued improvement is creating a divergence in strategy across the market. Smaller schemes (typically under £100m) are expected to increasingly move towards insurance solutions over the next decade, while larger schemes have a broader range of options, including running on, surplus release and consolidation solutions.

Recent developments, including the Pensions Bill which is expected to receive Royal Assent in May, are likely to accelerate consideration of surplus release options. An example of a surplus release solution is the Aberdeen-Stagecoach transaction, where trustees, advised by PwC, secured an additional uplift for pension scheme members.

Saye Mkangama, Pensions Partner at PwC, said: “We’re seeing a clear fork in the road emerging across the DB pensions landscape. Strong and resilient funding positions mean that many pension schemes are now able to make the strategic decision about their endgame with confidence. For smaller schemes, insurance buyout remains an attractive and increasingly accessible option, and we expect over the next five years or so most smaller schemes to choose that route when affordable to do so.

“For larger schemes, the picture is more nuanced. With improving funding levels and regulatory change imminent, trustees and sponsors are choosing between a wider set of options including running on, surplus release and alternative consolidation routes such as superfunds.

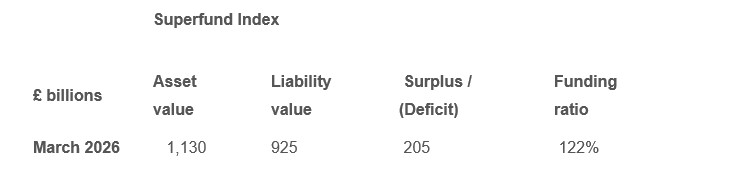

“What’s particularly notable is that superfund pricing is now broadly in line with low dependency funding, which could make it a more compelling option for some schemes. Overall, the direction of travel is clear: larger schemes are moving from repairing deficits to actively deciding how best to use and manage surpluses over the long term.”

The PwC Low Dependency Index and PwC Buyout Index figures are as follows:

|