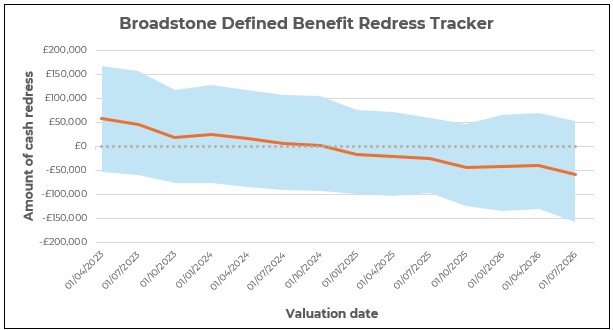

The quarterly Defined Benefit (DB) Redress Tracker from Broadstone provides an indicator of the level of compensation due to those who were previously ill-advised to transfer out of their DB pension.

Broadstone’s DB Redress Tracker follows the example of an individual who left their scheme in 2018 aged 50, with a pension of £10,000 p.a. which would receive inflation-linked increases when in payment. The potential spread around the example case has been updated to reflect the largest loss and gain in a notional portfolio of cases (previously it showed a narrower spread based on varying the fund return for the single example case).

The Tracker is developed in line with Financial Conduct Authority (FCA) rules for calculating redress with the individual assumed to have invested their funds to earn returns in line with the FTSE UK Private Investor Income Total Return Index.

The most recent update for Q3 2026 finds that a clear gain continues to be expected in most cases meaning that no redress is payable as the consumer is judged to be better off as a result of transferring. The central estimate for Q3 2026 is a gain of £59,000, markedly higher than the gain of around £40,000 in the tracker for the previous three quarters.

The increase in the gain has largely been caused by strong investment returns over Q2 2006 and a reduction in future inflation expectations which lowers the calculated value of the DB benefits given up on the pension transfer.

The last time that the Tracker found compensation would be payable was Q4 2024 (c.£2,000) with the central estimate showing a clear and sustained downward trend over recent times. Just over three years ago, when the current FCA rules were introduced, the central estimate found that c.£56,000 (Q2 2023) would be payable.

The central result hides the fact that there will be cases which do result in a loss which would mean that redress is payable. The reasons why a case might result in a loss are varied but typically arise from unusual investment strategies post transfer or older transfers (for example, before 2010).

Simon Robinson, Senior Consultant & Actuary in Broadstone’s Insurance Advisory & Remediation division, commented: “Markets experienced a quarter of significant volatility following the conflict in Iran, yet strong investment returns and a reduction in inflation expectations following an uneasy truce in the Middle East saw redress levels fall further. With DB transfer redress falling further, our central estimate continues to find that in the majority of cases, compensation would not be payable to consumers given the expectation of an increasing gain since their transfer.

“It is important to note that this estimate will not be uniform across all consumers. In some cases, factors such as investment performance or the time of transfer, for example, may result in redress being payable. It means that firms must remain diligent and asses each claim on its own merit rather than assuming no compensation will be due, despite the overall significant downtrend in redress calculations.”

|