By Mathilda Hobbis, Investment Consultant. Mercer

If we narrow the lens to consider the investment aspects of a DC default strategy in some of the largest overseas DC markets, it is clear that there’s no particular global consensus on the best approach to adopt (despite appearing to be broad agreement on the overarching objective to help members achieve income adequacy and sustainability throughout retirement). Notably, the Australian government is currently working to enshrine in law the purpose of their superannuation system with the proposed objective being to “preserve savings to deliver income for a dignified retirement, alongside government support, in an equitable and sustainable way”1.

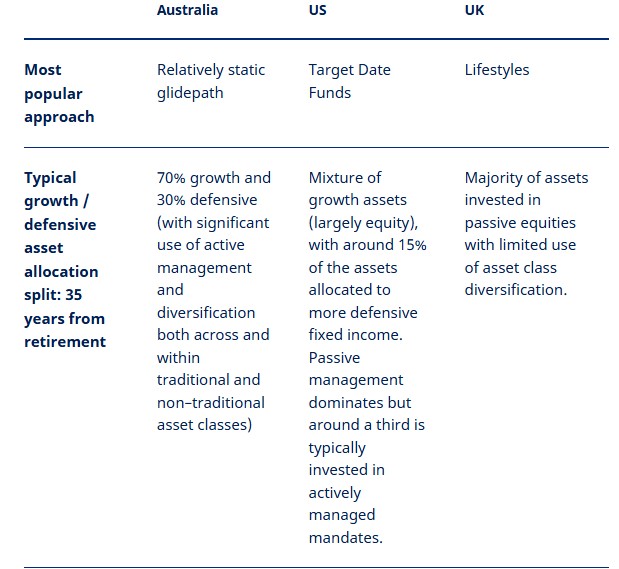

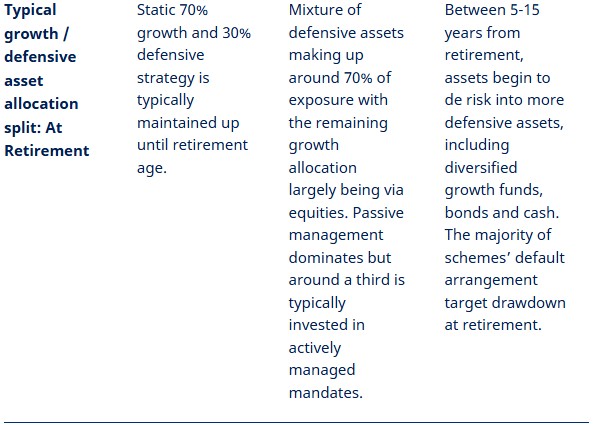

From an investment perspective, it is apparent that what emerges as typical best practice (or at least the industry standard) in any given region tends to be heavily influenced on how that particular market has evolved over time, as the disparity across regions highlighted by the table below demonstrates.

Source: Mercer internal research.

It’s worth noting that, despite the significant changes experienced by the UK DC market since the introduction of auto enrolment, it is still relatively new when compared to the more mature DC markets such as Australia and the US. For example, the Australian superannuation system is now 30 years old and an astounding A$3.5 trillion (£1.9 trillion) in DC assets. Given a population of just 26 million – it is a great deal larger than that of the UK in asset size, for less than half of the population2. The Australian DC market has also benefited from a much higher minimum contribution rate (12% from 2025 versus a UK rate of 8% of qualifying earnings for auto enrolment), albeit the minimum contribution in Australia did start out lower at 3-4% in 1993.

These factors combined mean that different region specific norms and constraints have evolved when it comes to designing DC defaults in each of these countries. This emphasises how there is no ‘one size fits all’ approach to default design. However, we can still learn a lot from other DC markets across the globe when we look to designing the defaults of UK schemes. In particular, through utilising Mercer’s capabilities for DC in the global context we can design the solutions in the UK which aim to provide better member outcomes. One notable example of this is the use of illiquid assets in the Australian market – where defaults typically have around a 15-20% allocation to illiquid assets. Clearly, in the UK there is a long way to go before the majority of schemes adopt a material allocation to illiquid assets, however we can take learnings for the Australian market when we look to consider some of the benefits and challenges of investing in illiquid assets and ultimately how this could help drive better outcomes for members in retirement.

(1) Mercer CFA Institute Global Pension Index 2023

|