|

|

Over the last decade, we have seen a significant shift in the defined contribution (DC) pension industry in the UK. The DC market has consolidated: own trust pension schemes have been in decline (and to a lesser extent contract-based schemes too), with Master Trusts emerging as the main beneficiaries. Today, around 3 in 10 employers (28%) provide pension plans using a master trust arrangement and, with government policy aiming to enable a small number of DC megafunds, this momentum towards consolidation is only likely to grow. |

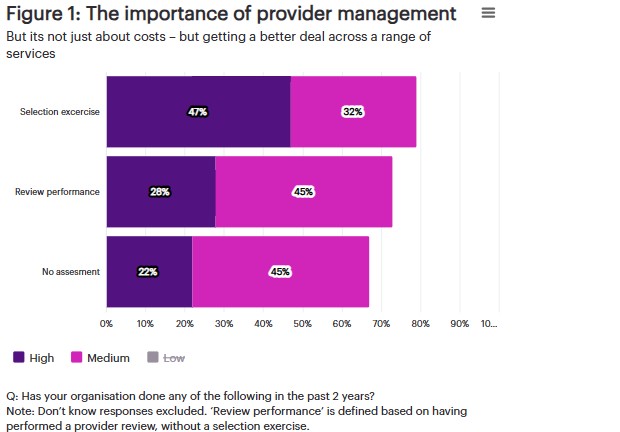

By Stuart Arnold, Director, Retirement and Claire Murray, Senior DC Consultant, WTW Alongside this trend, we see greater reliance on provider-designed investment strategies and less use of strategies designed by employers or pension trustees. With these changes, we see an increasingly cost-competitive environment. Annual management charges (AMCs) have declined from an average of 38 bps in 2017 to 28 bps in 2025, and today nearly 2 in 3 employers (61%) have AMCs less than 30 bps. This is against an emerging desire from Government and policy makers to focus more on value, rather than cost. Yet, even with charges at historic lows, our 2025 WTW DC Pensions and Savings Survey finds companies are still ambitious to get more value from their benefits and to use the retirement plan as a tool to attract, retain and engage their workforce. However, with very limited movement in average contribution rates in the last decade and no indication employers intend to increase them in the future, it seems employers aren't looking to spend more; instead, they are focussed on driving an improved deal from their providers and enhancing the experience and support they offer employees. Here are four things employers can do to add value now. 01. Assess value – are you getting a good deal from your provider? Assessing value is more than just charges, it means looking at the performance of the investment strategy and the effectiveness of delivery across the range of provider services. For many companies, getting a good deal increasingly means enhancing the services, support and experience employees receive. However, in today's competitive landscape, the most straightforward step to deliver value is to look to extract a better deal from providers. Especially for companies that haven't assessed the deal they are getting from their provider recently, it may be time to do so. In our survey, we can see that among companies that've been with the same provider for 10 years or more, nearly half (45%) report AMCs of 30 basis points or greater. For companies that have changed providers in the last five years, less than a quarter (23%) report AMCs this high. In the survey, we also asked companies to rate the value they receive from their provider across a range of metrics (value-for-money, the quality of communication material and digital tools, the range of investment options, the financial wellbeing and education support and at-retirement services). Based on these ratings, we categorised companies into three groups (low, medium and high) according to how highly they rate the effectiveness of their provider. Figure 1 highlights the importance of provider management (both selection exercises and regular reviews) in getting value from providers. Where a selection exercise has been done in the past two years, 47% report their provider is highly effective, compared to 28% for those who have run a recent performance review and 22% where neither have occurred.

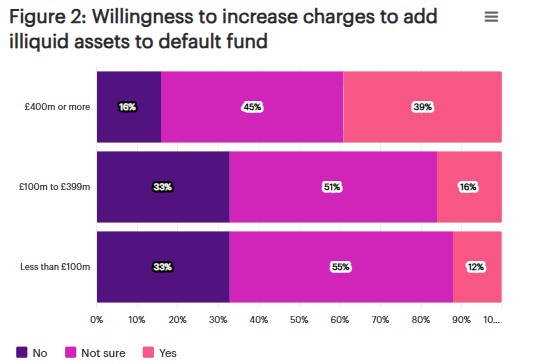

Interestingly, average AMCs are not particularly different across these cases. So, value is being driven from getting a better deal across the range of services, rather than just driving down costs. 02. Is it time to change course on investment strategy – can DC schemes do more to 'go for growth'? In recent years, DC schemes have increasingly moved towards low-cost off-the-shelf default strategies, with passive investment approaches becoming the norm. This reduction has sparked some debate: has there been too much emphasis on keeping costs down and not enough attention paid to investment value? Can value-for-money be improved by accepting higher charges and by 'going for growth' through accessing alternative investment strategies? With the UK government, through the Mansion House Compact, seeking to encourage greater investment in these asset classes, whether illiquid assets, such as private equity or infrastructure, hold the potential to enhance returns is a key debate in the pension industry. To explore employer perspectives on this topic, our survey asked employers whether they were willing to increase annual management charges to be able to add illiquid assets to their default fund (Figure 2).

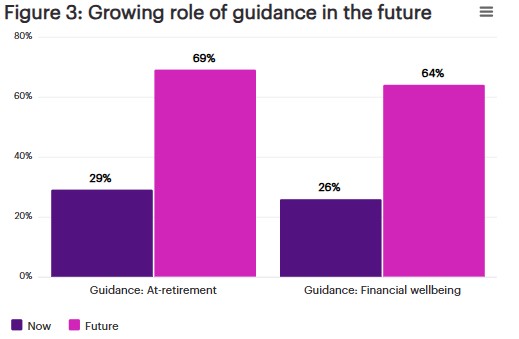

Employers with larger DC schemes are more willing to accept higher charges to access illiquid investments (39%). This may be due to the fact that they have already been very successful in driving down charges, or that their pension scheme has the scale and buying power to effectively access these assets. By contrast, only a small number of companies with smaller and medium-sized pension schemes are willing to do so, albeit many remain undecided. Across all cases, the amount companies are willing to raise annual charges to access illiquid assets is moderate (an additional 10 bps on average). Hence, while there is interest in enhancing the role of alternative investment strategies in DC default funds (particularly for larger schemes), there is also some caution among companies. Employers should look to understand what their provider is doing now and their plans for the future (and at what cost). Providers have been evolving their defaults to address private markets integration; nevertheless, implementation varies widely by provider. Now is the time for employers to reassess their investment strategies to ensure their provider's solution is appropriate. 03. New thinking on decumulation As DC matures and employees become increasingly reliant on their DC pensions, we are seeing a growing focus on decumulation strategies and how to deliver greater value to members as they draw on their retirement savings. This focus is being accelerated by Government legislation, which will place new requirements on pension schemes to identify and offer suitable retirement income products to members approaching retirement (Pension Schemes Bill 2025). These new rules are expected to apply from 2027 for Master trusts and from 2028 for other DC trust-based schemes and Group Personal Pensions (GPPs). By this time, schemes will be required to have in place a decumulation strategy that meets member needs, provide a justification for their approach and communicate to members about the default pathways. The window to develop these default pathways is then small. For employers, the first step is to understand what their scheme or provider is doing. However, the bigger question is whether this represents an opportunity to take a more fundamental look at what solutions best meet the needs of employees. Against this backdrop, we are seeing more innovative thinking about potential decumulation strategies. The Institute for Fiscal Studies (IFS) and NEST have discussed approaches that look to 'flex then fix', where employees manage, say, the first 10 years of retirement via drawdown, but then purchase an annuity as they reach, say, 75. Others are discussing the use of deferred annuities. Common to these approaches is a desire to bring back a greater degree of retirement security, longevity protection and to make it easier for employees to manage their money in retirement as they reach their old age. We also continue to see ongoing discussions on collective DC (CDC) as an alternative approach, both with regards to accumulation and decumulation. Indeed, around 5% of employers in our survey are considering a switch to CDC as a plan vehicle. Decumulation strategies are then once again on the agenda and whilst there is no one clear direction of travel yet, it's an area we expect to see significant change in the decade ahead. 04. Adding value by enhancing the employee experience and helping employees make better decisions For most companies today, their top priority is to improve the employee experience, help employees better understand their plan and support them to make better decisions. These are long-standing challenges, but new solutions are emerging that offer real promise to shift the needle, particularly in strengthening financial wellbeing and at-retirement support. Increasingly, we see companies looking to provide (and pay for) access to additional guidance to their employees. Guidance services stop short of full financial advice, but offer more cost-effective means to support workers, both as they approach retirement and to support general financial wellbeing. For many companies, guidance is the appropriate level of support an employer should provide (offering options and support, but without providing direct recommendations). Today 3 in 10 employers provide or facilitate such services and this could potentially increase to 7 in 10 in the next few years (Figure 3).

In this fast-developing field, where we see web tools, online and face-to-face services becoming available all the time to support members, employers should review what their scheme provides and what is available, including how these services are funded.

Final thoughts But it's not just the costs. Employers continue to reframe their plans around what employees need, prioritising stronger support, clearer guidance and a more engaging employee experience at key moments that matter. The challenge is then to drive enhanced value across the full range of investment strategies, at-retirement support and member engagement. At WTW, we work with a wide range of employers and trustees to navigate these challenges — helping them design retirement strategies that are fit for purpose and fit for the future. We support employers and trustees in their governance, and monitoring and managing their provider relationships, to deliver value to both employers and employees. If you would like a personalised benchmark summary to understand how your organisation's situation compares to others and to examine the trends outlined above in more detail, please participate in the survey today. |

|

|

|

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd