Last month, we wrote that markets were stumbling towards resolution in Iran, but that the process was likely to follow a two-steps-forward, one-step-back dynamic. Unfortunately, the past month has delivered rather more of the latter than the former. We still see a path to resolution, but it has become increasingly obscured.

The direction of global bond yields (yields move inversely to price) has tracked energy markets extremely closely and for now we see little reason for that relationship to break down. Swings in oil and gas prices are therefore likely to remain the primary driver of global yields in the near term.

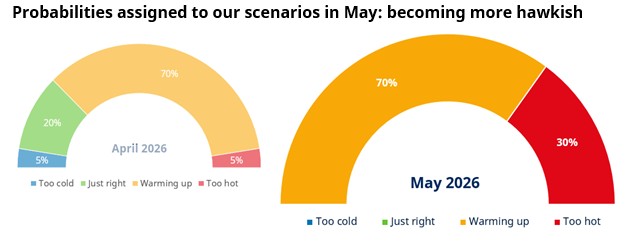

This is reflected in the probabilities we assign to our scenarios. In light of global inflation dynamics, we now place a zero weight on the two most dovish scenarios (“Too cold” and “Just right’). On balance, we still expect the US Federal Reserve (Fed) to keep interest rates on hold - as captured by our “Warming up” scenario - but now see a higher chance of rate hikes (“Too hot”), although our expectations of this outcome are lower compared to the market.

Source, Schroders Global Unconstrained Fixed Income team 20 May 2026, for illustrative purposes only. The “too cold" scenario would see the Federal Reserve (Fed) cutting 4+ times in 2026, 2-3 cuts for “just right", while in “warming up” the Fed is only cutting once or is on hold. Finally, in a “too hot" scenario the Fed is moving back towards hikes in 2026, because inflation is becoming problematic again.

Relatively speaking

The US economy continues to perform well. Most importantly for the US monetary policy outlook, the weakness we’ve seen in the labour market is now more clearly behind us. Unlike many other central banks, the Fed’s mandate includes “full employment”, so this improvement removes one of the key reasons the Fed has to lower interest rates from here.

The baton driving growth has now been handed to the business community. The significant improvement in the manufacturing sector is partly linked to the surge in technology investment - linked to the AI revolution – however, we’re seeing this improvement broadening into other sectors. This is not a new theme, but it has gained traction in recent months.

Meanwhile, the real income squeeze due to higher inflation is being partially offset by fiscal stimulus (President Trump’s “One Big Beautiful Bill”) albeit there’s winners and losers through this and we are starting to see evidence of stress among lower-income households. Taking all this together means that we still see US Treasuries as less attractive compared to peers.

What we’re doing and what we’re watching

Instead, we continue to see opportunities for long exposure in Canadian and Australian rates markets. For Canada, our story is unchanged. The economy was soft ahead of the war in the Middle East and we see the rate hikes priced into bonds over the next 12 months as being inconsistent with this. The latest labour market data, with net job losses in March and weak leading indicators, only reinforces this view.

The outcome of May’s Australian Federal Budget (2026-27) helped solidify our conviction for Australian bonds, with overall fiscal policy moving from stimulative to neutral. The Reserve Bank of Australia (RBA) has already tightened policy three times and while another hike remains more likely than not, the end of the cycle is now coming into view. That’s always a pivotal moment for bond markets.

Elsewhere, we remain neutral on duration (interest rate risk) in the eurozone. Unless we see a sharp fall in energy prices, we expect to see the European Central Bank (ECB) raise interest rates in June. However, with almost three hikes priced for the rest of the year we see little asymmetry on offer: bonds will rally if energy prices come down, but with a central bank that’s alert to inflation risks, will sell-off more if they don’t.

We also have a neutral view on UK duration, given the market’s high sensitivity to global energy dynamics as well as the rise in political uncertainty in recent weeks. For now we think it prudent to stay on the sidelines and wait for a clearer opportunity to arise.

From an asset allocation perspective, our view is broadly unchanged on the month. We remain cautious on corporate credit due to unappealing valuations, but continue to see opportunities within emerging market debt and peripheral eurozone markets (for example Greece).

|