Product sales data from the Financial Conduct Authority (FCA) shows a trend of fewer pension savers taking advice when buying income drawdown and guaranteed income for life solutions.

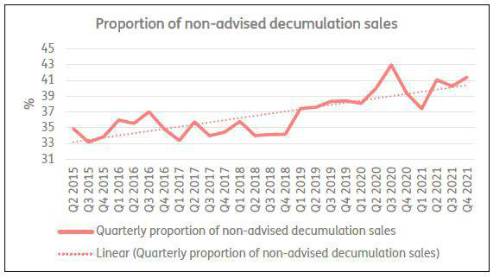

Analysis from retirement specialist Just Group shows that 104,774, or 40%, of the 262,261 decumulation products bought in 2021 were purchased without professional, regulated advice.

This was the highest number of sales of non-advised decumulation solutions since the pension ‘freedom and choice’ reforms of 2015 and highlights that non-advised purchases have been trending higher from a low of one in three (33%) in 2015 to more than four in 10 (41%) in the last quarter of 2021.

“The long-term trend has been a decreasing use of advice by consumers when they are making complex choices around how to use savings to fund retirement,” said Stephen Lowe, group communications director at Just Group.

“We know only a minority of these non-advised customers take up their entitlement to free, independent and impartial pensions guidance, so these figures paint a troubling picture of more people making long-term retirement decisions every year without any professional advice, help or guidance.”

The FCA’s product sales data only includes sales of decumulation products – guaranteed income for life and drawdown plans. It doesn’t include the 300,000+ defined contribution pensions that are fully withdrawn each year, typically by people not taking either advice or guidance.

“We are now seven years on from the ‘freedom and choice’ reforms and take-up of professional advice and free guidance is going backwards – surely this can’t be what the government had in mind?” said Stephen Lowe.

“We’re talking about large sums here – an average of around £67,000 for each pension used to buy a guaranteed income for life plan and more than £156,000 for the average drawdown solution.

“It’s inevitable that without advice and guidance some people will make decisions they’ll come to regret and much more needs to be done to stop so many continuing to fall through the cracks in the advice and guidance framework that the government and regulator have put in place.

“Pension Wise is the lifebelt George Osborne promised every saver when pension freedoms were announced but only the rare few get it. Evidence given to the Work and Pensions Committee by the Money and Pensions Service (MaPS) found that an earlier nudge – before people have made up their minds to access pension cash – is more effective in getting people to Pension Wise.

“But it seems the longest-serving pension minister and the FCA are content to let people flounder their way into retirement and not even trial this.”

|