“Suggestions that the LISA will undermine pension savings are, we think, overdone. The idea that people will opt out of pensions to save for house purchase in a LISA seem to confuse cause and effect.Those who are determined to buy their own home but can’t afford to do that and contribute to their workplace pension will surely opt out of the pension in any case. The LISA just gives them a product that they can do that in more tax effectively allowing them to get back into retirement saving sooner.

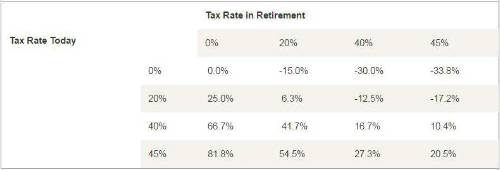

“Beyond this, it will clearly remain best advice for people to stay in their workplace pension and get any employer contribution available to them. But saving in a pension beyond this level may be questionable. Generally anybody paying basic rate tax today will be better off making additional saving in a Lifetime ISA rather than saving in a pension. The government subsidy to the LISA gives savers a 25% uplift whereas pensions will provide only a 6% uplift for those still paying basic rate tax in retirement and those who become higher rate payers actually lose 12.5%.

“The situation for those paying higher rate tax is more complex. Those who expect to be basic rate payers in retirement should stick with the pension as this will give them a 42% uplift on their original saving whereas those who will remain higher rate payers will be slightly better off (7%) in the LISA.

“It has to be remembered that the LISA is only available to those under 40 and is limited to £4,000 of savings a year. Older savers with more to invest will still find pensions the best option.

“Overall then we see the Lifetime ISA as a valuable addition to the savings landscape. It will make a meaningful difference for younger savers who value flexibility and for whom the current system of pension tax-relief offers little.”

Table: Comparing Pension and Lifetime ISA – Uplift from Saving from Taxed Income into a Pension

|